One Way to Get Rewarded for Investment Risk: Hold on When Prices Falll

By: Thomas Anichini, GuidedChoice

The next time you feel tempted to sell because the market is falling, keep in mind the risk of losing money is what investors get rewarded for taking.

- The risk-reward relationship compensates investors for risking loss.

- When taking risk doesn’t feel frightening, the reward tends to be muted.

- Instead, investors tend to be rewarded for taking risk when it feels scary to do so.

(Note: this article is adapted from a GuidedChoice blog post from 2018).

While we never know when the market will experience turmoil, we know periods of market turmoil are inevitable. At times like now, when investors are not panicking because prices have mostly been rising, it’s worth revisiting how risk and reward actually work. This perspective can help you talk members out of making panicked decisions during the next inevitable period of market stress.

Pay to Avoid Losses; Get Paid to Endure Them

People do not like to lose wealth! Many people are willing to pay to avoid losses, which is why insurance exists as a profitable business. Insurers earn a profit by pooling people’s risks and absorbing catastrophic losses.

While investing in stocks isn’t the same as underwriting insurance, there is one economic similarity: If you are unwilling to withstand losses, you will have to pay a premium. If you are willing to withstand them, you should expect to earn a premium.

It is easy to hold stocks when prices are rising. It feels good and it feels smart. However, the advantage to holding stocks arises mostly when more people are afraid of holding them.

Growth Isn’t Smooth

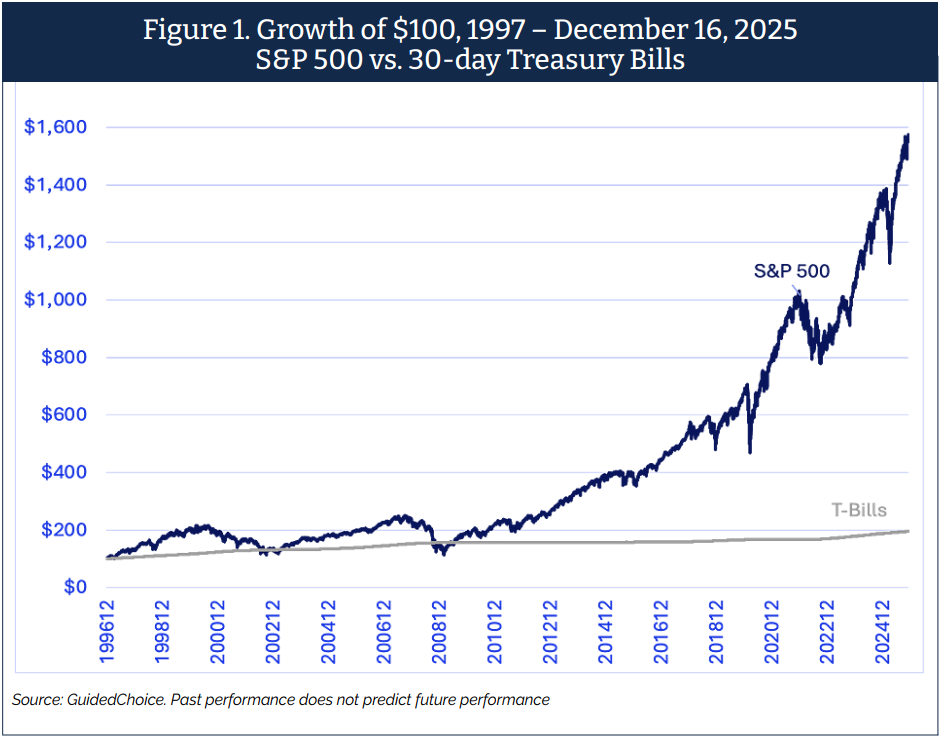

Figure 1 compares the growth of $100 invested at the end of 1996 in the S&P 500 Stock Index to the growth of $100 invested at the end of 1996 in 30-day US Treasury Bills.

Notice how jagged the Stocks line is and how smooth the Bills line is. What we want is the growth from Stocks with the smoothness from Bills. But financial markets don’t work that way. Basic risk–reward logic tells us that an asset with a growth path as comfortably smooth as TBills should not earn a risk premium, and indeed TBills do not. By contrast, investors willing to endure the stock market’s jagged rough patches expect to be rewarded over the long term.

High Returns Tend to Follow Poor Ones

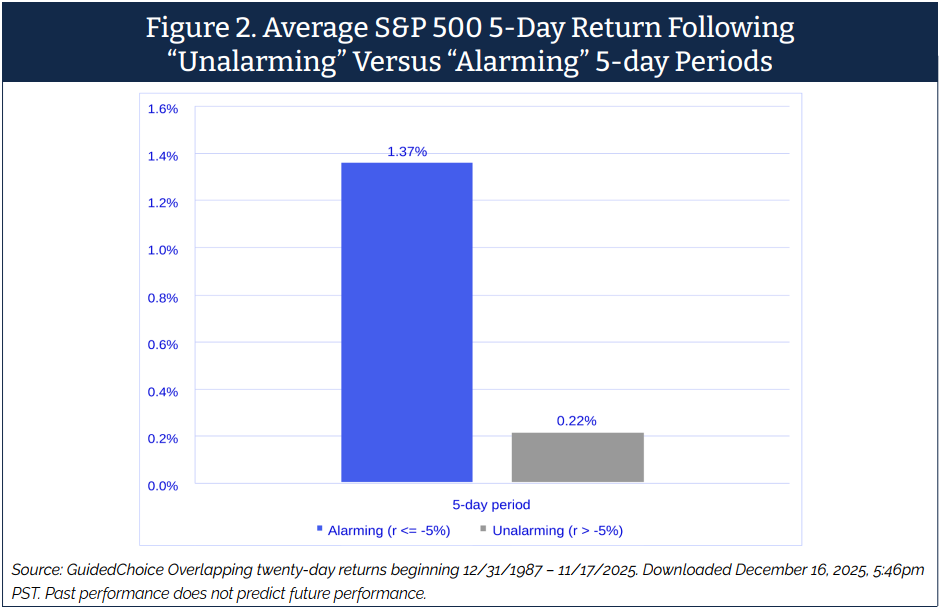

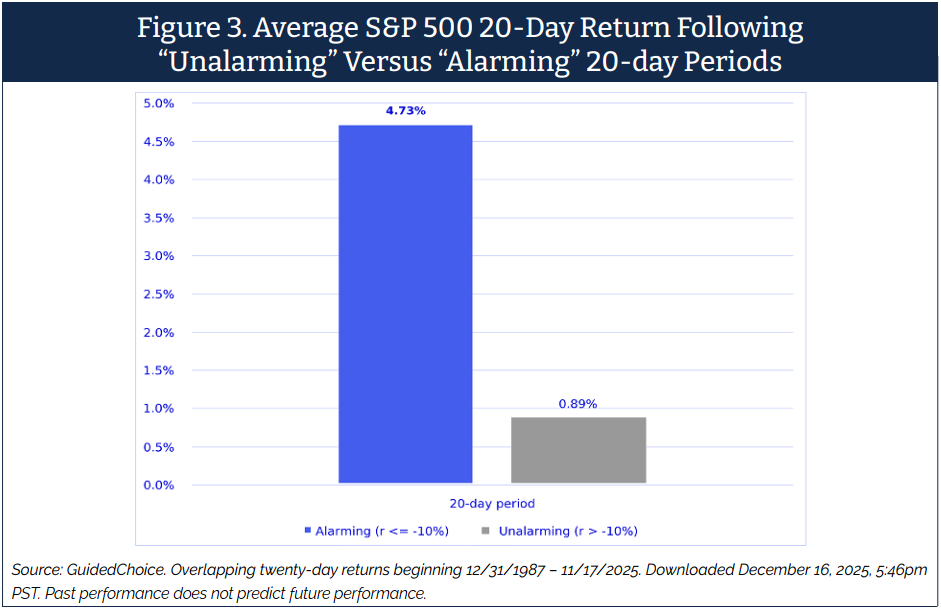

Let us examine how the market tends to behave following periods of alarming losses. For this purpose, we group 5-day periods when the S&P 500 loses 5% or more “Alarming,” and apply the same label to 20-day periods when it loses 10% or more.

Figure 2 shows that on average, since year-end 1987, following a one-week loss of 5% or more in the S&P 500, investors have earned 1.37% over the next week. By contrast, following unalarming weeks they earned only 0.22%.

Figure 3 shows that on average, since year-end 1987, following a one-month loss of 10% or more in the S&P 500, investors have earned 4.73% over the next month. By contrast, after unalarming months, they earned only 0.89%.

These are merely averages; they do not mean that losing money automatically signals an imminent rebound. What they do mean is that investors need to calibrate the amount of stock they hold to their time horizon.

This is why an important variable in determining how much a person should allocate to stocks depends on how long before they need to withdraw from their portfolio. They should calibrate the probability and size of expected losses according to their time horizon. The bargain they make when they invest in a diversified portfolio of stocks is simple: they are expecting to earn a premium for being willing to withstand occasional short-term losses. But once they’re calibrated, leave it alone (save for occasional rebalancing).

Members who are within about 10 years of retiring should check with a professional on an appropriate allocation to stocks for their remaining saving horizon. For members investing for more than 10 years before withdrawals, the day-to-day market level matters far less than whether they are saving enough. In many cases, it may be better to delay withdrawals, if possible, rather than reduce stock exposure in a panic.

About the author: Thomas Anichini, CFA, CFP is Chief Investment Strategist with GuidedChoice / 3Nickels, with over 30 years of actuarial and investment experience.

Tom is a member of GuidedChoice’s Investment Committee. He refines GuidedChoice’s capital market assumptions and proprietary return model, and also contributes to GuidedChoice’s retirement advice engine and 3Nickels financial advice engine. Tom communicates about the firm’s philosophy and advice, and represents the investment team when facing clients and consultants.

Prior to joining the firm, Tom gained experience in various actuarial, investment consulting, and portfolio management positions, including for EnnisKnupp & Associates, Mercer, Westpeak Global Advisors, and Freeman Investment Management.