Resource Crunch: Why Efficiency is a Smart Bet in a World of Rising Costs

As the costs of raw materials, energy, electricity, and water surge, scalable products and services that enhance resource efficiency have become attractive investment opportunities for pension funds.

Executive Summary

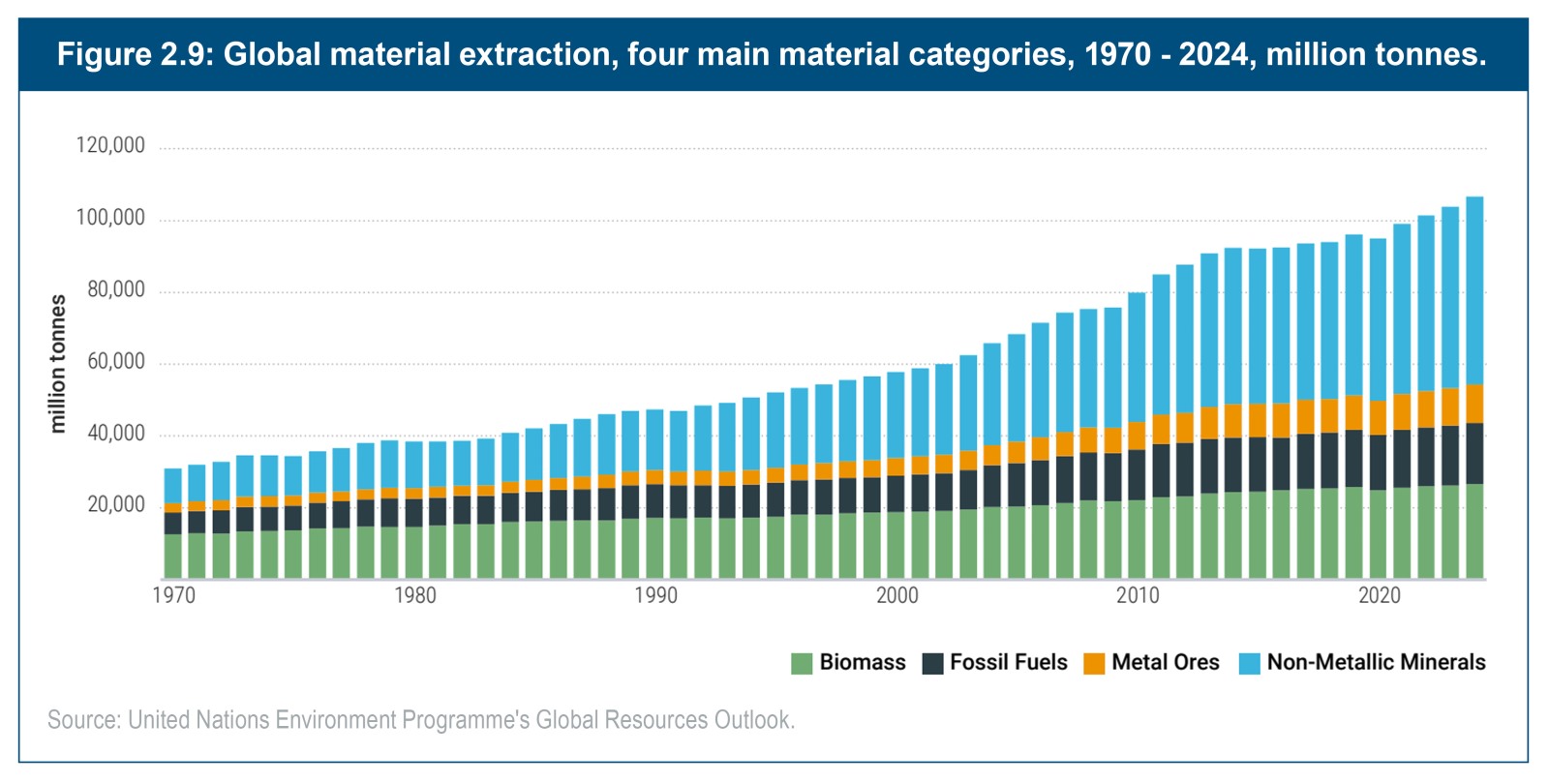

Demand for raw materials has tripled over the last 50 years and still grows ~2.3% annually. As costs for energy, electricity, water, and other inputs rise, companies and governments face growing pressure to use them more efficiently.

This shift is reversing decades of declining real prices, accelerated by regulatory mandates and climate goals. In parallel, a wave of enabling products and services—from IoT sensors and AI analytics to advanced recycling and pyrolysis—is making resource efficiency more scalable and cost‑effective than ever.

According to the International Energy Agency (IEA) and the Ellen MacArthur Foundation, circular economy, resource efficiency, and electrification markets may reach $3.4 trillion annually by 2030. Recycling and composting, waste‑to‑energy, smart water management, and biochar are expanding rapidly. These sectors offer strong financial upside while advancing resilience, circularity, and modernization.

Pension fund managers are uniquely positioned to capitalize on these trends. Mature efficiency solutions now deliver stable, predictable cash flows, downside protection via hard assets, inflation‑hedged exposure, and uncorrelated returns.

Private credit is increasingly financing resource efficiency companies. Where equity struggles with capital‑intensive solutions, private credit provides flexibility and speed to fill the gap. With tailored structures, private credit investors can access growth in efficiency plays critical to cost reduction and improved performance, while capturing attractive risk‑adjusted returns in underserved markets.

Rising Cost of Resources

Raw Materials

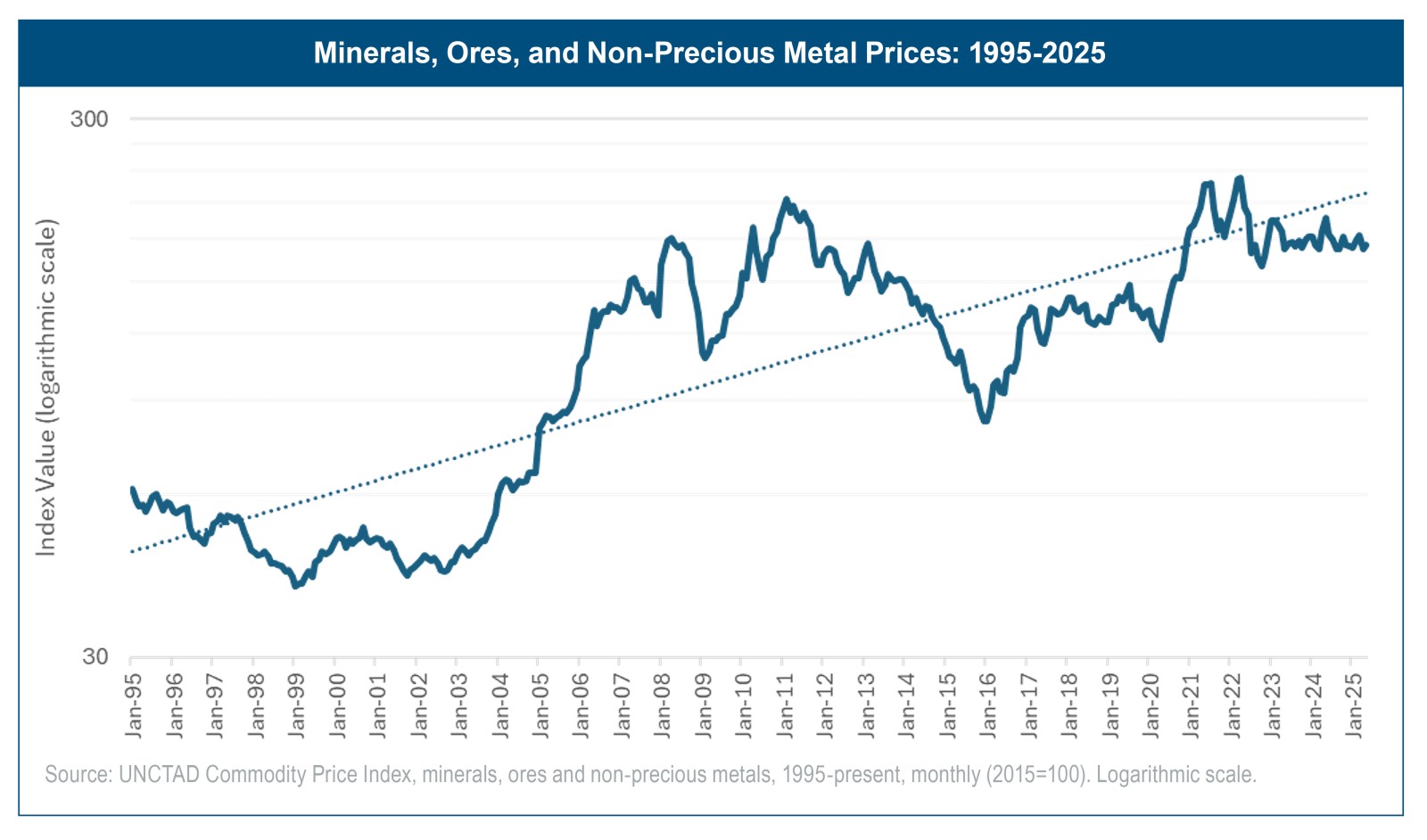

Throughout the 20th century, real prices for many raw materials declined, driven by productivity in mining and agriculture. Around 2000, the trend reversed: global raw‑material costs began rising. Since then, global raw‑material costs have been on a persistent upward trajectory. Industrial metals (copper, aluminum, steel) and critical minerals (lithium, nickel) have become markedly more expensive in the 21st century.

The last 30 years’ price surge is mainly demand‑led, tied to the energy and digital transitions. Lithium underpins batteries, copper enables electrification, and nickel and cobalt are essential for EV batteries and high‑performance alloys.

The last 30 years’ price surge is mainly demand‑led, tied to the energy and digital transitions. Lithium underpins batteries, copper enables electrification, and nickel and cobalt are essential for EV batteries and high‑performance alloys.

Energy and Electricity

Global energy prices have trended upward for two decades. After collapsing during COVID‑19, fossil fuel prices spiked to historic highs in 2022 on post‑pandemic demand and the Russia–Ukraine war. Although they have moderated, the IMF’s global energy price index in 2025 remains 66% above its 2016 baseline. Over time, supply chains have also become more complex and capital‑intensive. Long‑term costs are pushed higher by demand growth—especially in emerging markets—and by the rising expense of extracting and delivering supply from deepwater fields and LNG infrastructure. These dynamics reflect both cyclical shocks and structural forces.

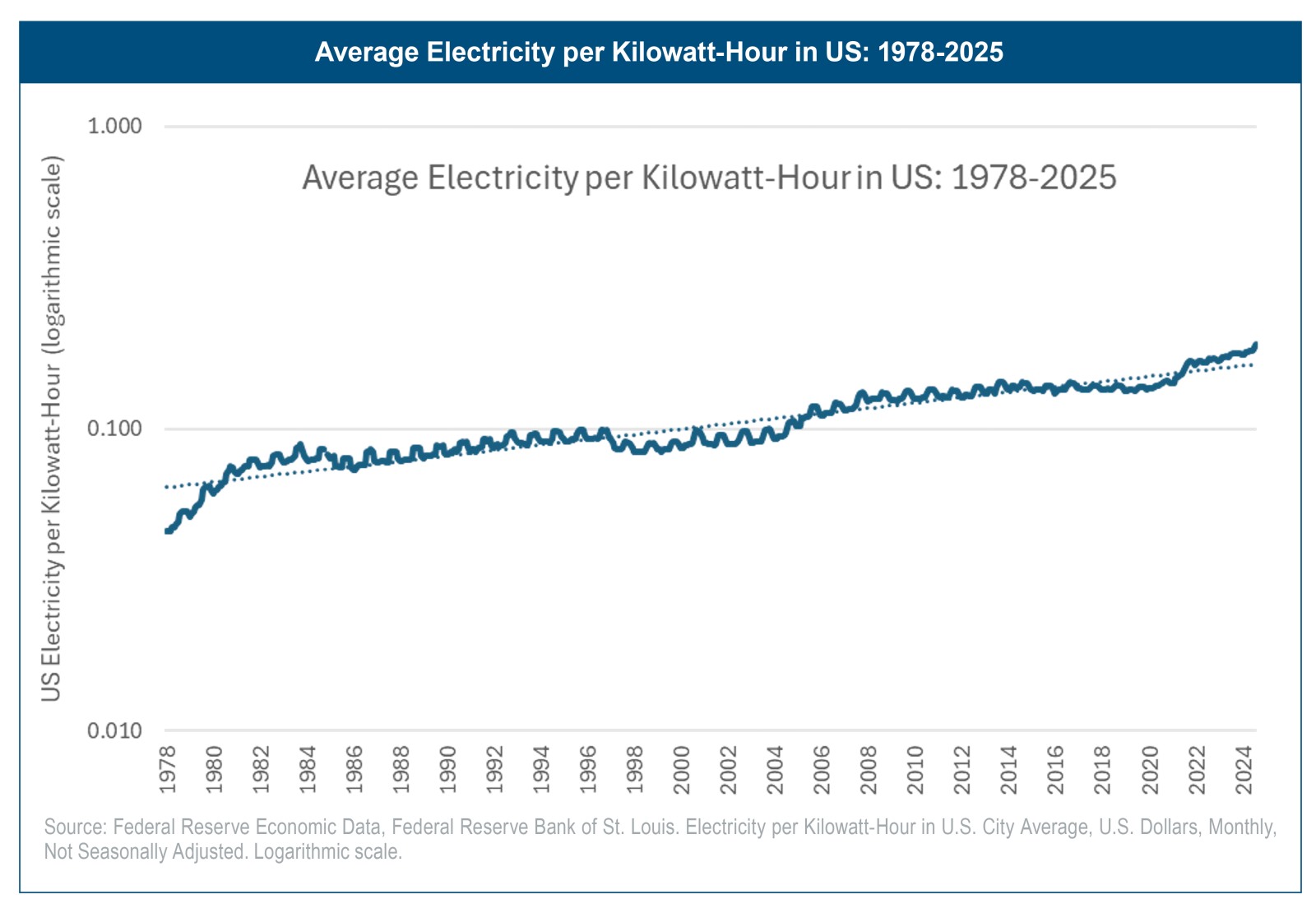

Electricity prices are climbing as well. After a relatively flat 2010s, U.S. electric bills are now rising. In 2024, retail power prices increased 3–4% year‑over‑year, outpacing inflation, and the U.S. Energy Information Administration (EIA) expects American households to pay a record rate in 2025.

Multiple forces are at work. Higher energy costs and heavy utility investment to replace aging transmission and distribution (T&D) and to connect renewable power generation sources are lifting bills. T&D now accounts for a growing share of costs, pushing prices higher even when fuel is stable. Supply disruptions—such as the 2021 Texas winter storm—add pressure. Meanwhile, electrification of transportation and heating is boosting demand; without matching supply, prices will keep rising.

Water

Water is typically delivered as a public utility at low, often government‑subsidized, prices, yet costs are increasing due to aged infrastructure, scarcity, and more expensive treatment. Global Water Intelligence reports the steepest recorded global tariff increase in 2023–2024, with average bills for water, wastewater, and stormwater up 10.7%.

This reflects a perfect storm of expenses: long‑delayed upgrades and expansions, climate‑resilience needs, and energy‑intensive operations that rise with energy and electricity prices. Treatment chemicals and construction materials (e.g., pipes) have also climbed, mirroring broader raw‑material trends. Climate change is driving investment in adaptive infrastructure, including flood protection and drought‑resilient desalination and water recycling.

Investment Opportunities

A wave of solutions is creating compelling resourceefficiency investments. Recycling and composting, wastetoenergy, smart water management, IoT/AI methaneleak detection, smart irrigation, and advanced pyrolysis reactors are becoming more affordable and scalable.

A detailed write up of each these investment opportunities and data sources is available here on the CurvePoint website.

Bios: James Rich is Managing Partner and Co-Founder of CurvePoint Capital, with 22 years of investment experience in private and public investments across diverse asset classes. Before co-founding CurvePoint, he spent 15 years at Aegon Asset Management, where he co-founded the Aegon Climate Capital strategy. He also served on the board of the Aegon Transamerica Foundation, supporting financial and social empowerment initiatives. Earlier in his career, James worked at Madison Dearborn Partners and Morgan Stanley. A frequent speaker and guest lecturer, he has been featured in the Financial Times, Barron’s, the Wall Street Journal, Bloomberg, and more. He mentors climate ventures through Third Derivative and holds an MBA from Kellogg and an ScB from Brown University. He lives in Boulder, CO with his wife and three children.

Disclosures: This document is being provided to you for informational purposes only and is not a recommendation of, or solicitation for, the subscription, purchase, or sale of any security. The information contained in this document is not intended to provide professional, investment, legal or tax advice and should not be relied upon in that regard. The contents of this document are for general information only and are not provided with regard to your specific investment objectives, financial situation, tax exposure or particular needs. The contents hereof are not a recommendation of, or solicitation for, the subscription, purchase, or sale of any security. Nothing contained herein should be used as the basis for making any specific investment, business, or commercial decision. You should read the final offering documents, limited partnership agreement and/or other supplemental and controlling documents before making an investment decision regarding any particular security carefully before investing in any security.

The document is being provided on a confidential basis solely to those persons to whom this document may be lawfully provided. It is not to be reproduced or distributed to any other persons (other than professional advisors of the persons receiving these materials). It is intended solely for the use of the persons to whom it has been delivered and may not be used for any other purpose. Any reproduction of the document in whole or in part, or the disclosure of its contents, without the express prior consent of CurvePoint Capital Management LP and its affiliates (“CurvePoint Capital”) is strictly prohibited.