A Differentiated Private Credit Approach in Today’s Competitive Environment

By: Javier Dyer and Greta Ulvad, EnTrust Global

This piece discusses how private credit investors can benefit from a differentiated approach to the asset class in today’s competitive market environment, in particular by targeting off-the-run, smaller loans to non-sponsored companies and being flexible in terms of borrower type, instruments, and collateral (both corporate and asset-backed lending).

The private credit landscape has grown more competitive in recent years as the asset class continues to attract capital, with large established players increasing scale and newer entrants emerging to compete for share. This has resulted in spread contraction and borrower-friendly terms across certain transactions. Against this backdrop, a more flexible and differentiated approach to capital allocation across market segments is needed to generate attractive returns.

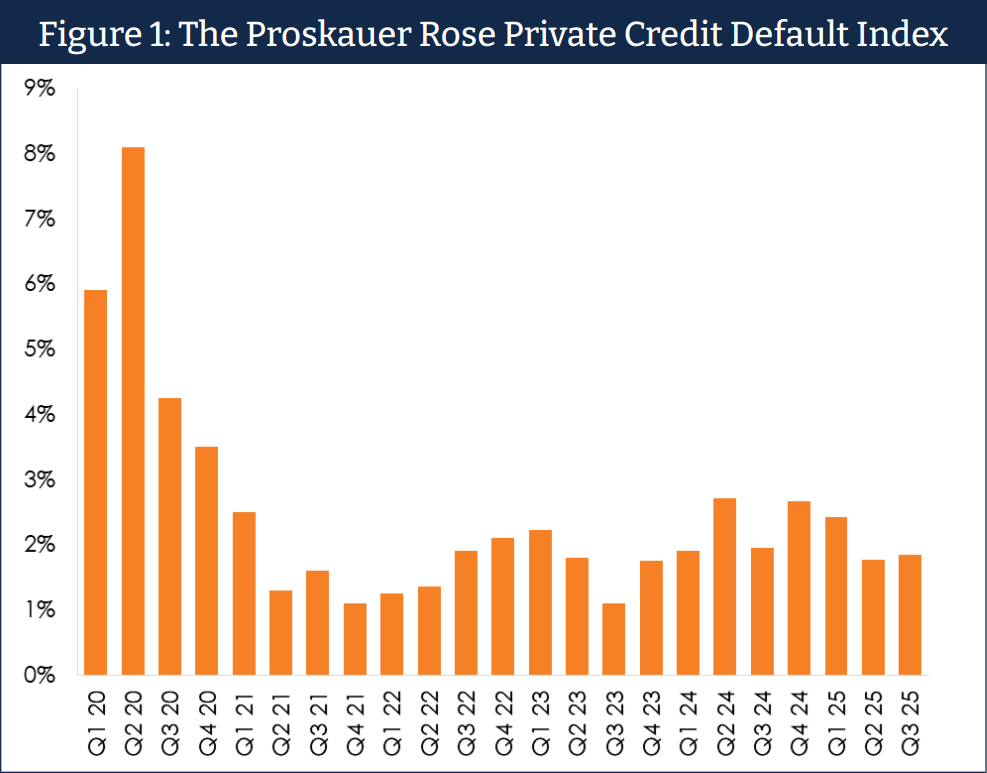

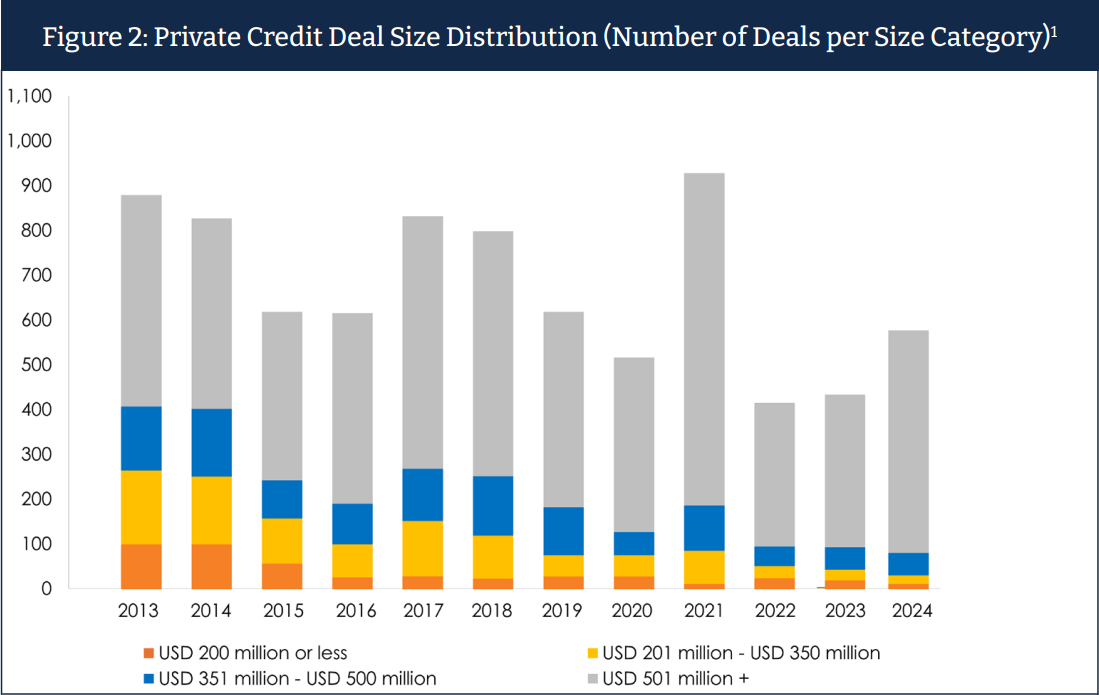

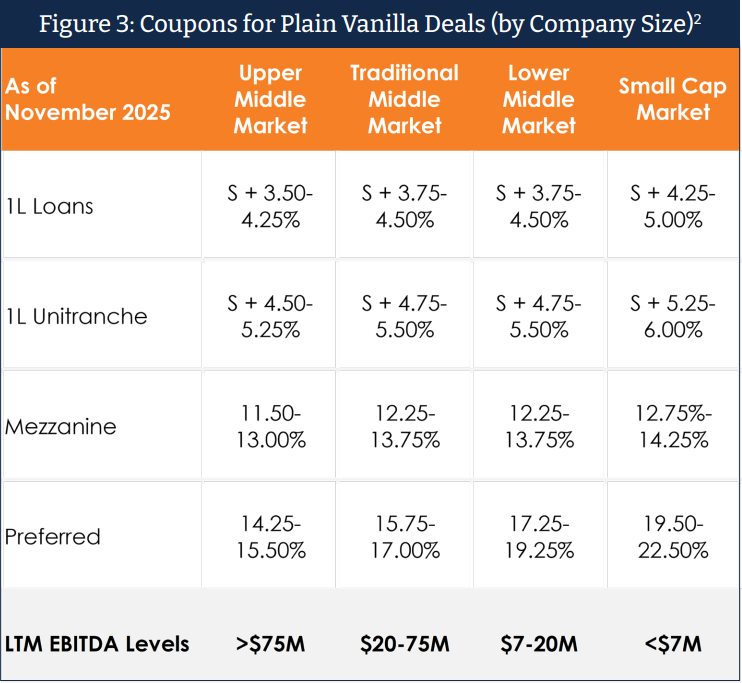

Despite a relatively benign default backdrop (Figure 1), concerns have been raised about a private credit bubble and the commoditization of returns in the space. To some extent, these concerns are legitimate: the assumption that the dramatic inflow of capital has relaxed the underwriting standards of market participants is evidenced by the recent bankruptcies of private credit borrowers Tricolor and First Brands. As capital continues to flow into direct lending, in order to compete with the broadly syndicated loan (“BSL”) market, large private credit participants have originated more covenant-lite deals. Moreover, concerns regarding lower returns are valid; however, commoditization of returns is also skewed toward larger, sponsor-backed deals. The direct lending category of private credit is where the bulk of the growth has occurred, with the traditional BSL market losing share as the dramatic inflow of capital has pushed the direct lending industry into making larger and larger deals (Figure 2). Financing large, plain vanilla transactions is turning into a volume business, which is weighing on returns (Figure 3).

We believe the commoditization of returns that has emerged across large, plain vanilla direct lending to traditional PE-backed sponsors can be avoided by structuring a private credit strategy with flexibility across types of borrowers, collateral, instruments, and structures. Specifically, we believe more off-the-run (including non-sponsored) and smaller loans, as well as wholistic capital solutions, can still generate attractive returns.

1. Non-Sponsored Loans

When it comes to corporate private credit, what typically comes to mind is lending to sponsor-backed companies. This makes sense given that (1) direct lending to sponsor-backed companies represents the lion’s share of the private credit market, and (2) the largest sponsor-backed loans, for amounts as high as $3B+, regularly make headlines. There are many reasons why lenders gravitate toward PE-run companies, including the sizable market opportunity provided by LBO financings, especially as direct lending has taken significant market share from the BSL market, and the institutional quality of corporate governance and financial controls often associated with PE ownership.

However, as many private credit participants restrict lending outside of sponsor-backed deals, many attractive non-PE corporate lending opportunities fall by the wayside, causing such companies’ needs to be underserved. Indeed, there are many high-quality founder-owned businesses, that — albeit of typically smaller size — are run professionally and profitably. When these companies seek financing, fewer lenders are interested in bidding for the business, which generally leads to a less competitive process and, in turn, creditor-friendly economics and covenant protections. Traditional direct lenders are typically not mandated to participate in non-sponsor-backed situations, creating opportunities for flexible private credit investors who are agnostic to borrower type.

2. Smaller Loans

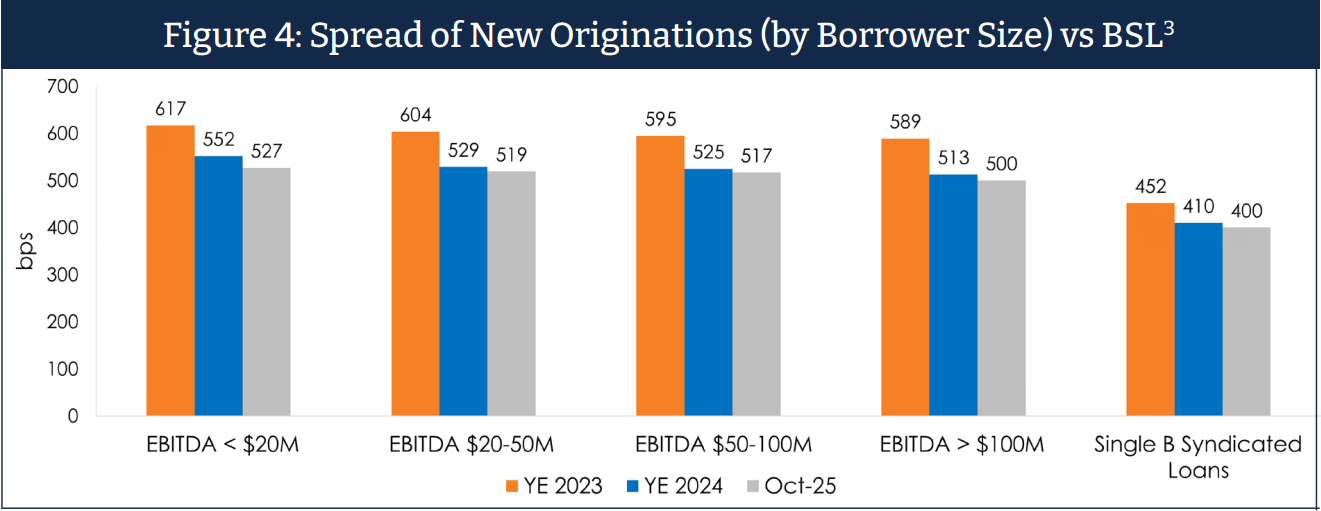

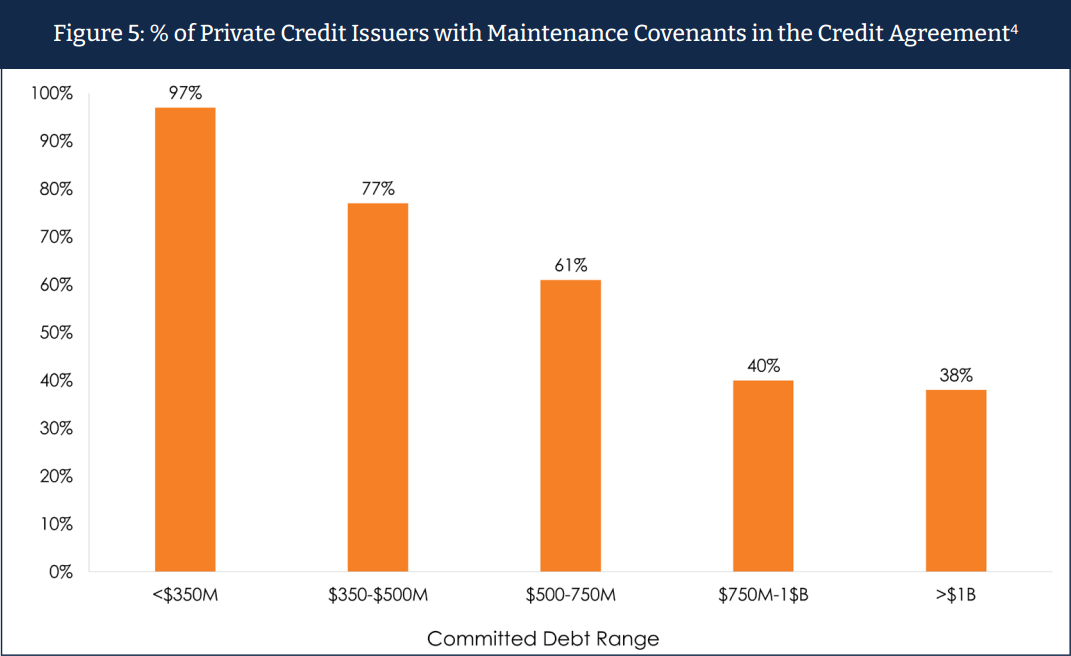

Competition is much lower for loans in the $200–500M range – which are generally to smaller companies – where lenders can negotiate for better pricing (Figure 4), as well as more restrictive covenants. Indeed, while $750M+ issuances more closely resemble the covenant-lite nature of the BSL market, with only ~40% of such transactions featuring maintenance covenants, the majority of issues in the $350–$500M category and nearly all of deals less than $350M have maintenance covenants (Figure 5). Moreover, smaller loans generally involve tight/aligned lender groups, which minimizes the risk of disruptive creditor-on-creditor violence and disagreements over amendments and other situations requiring lender flexibility.

3. Capital Solutions

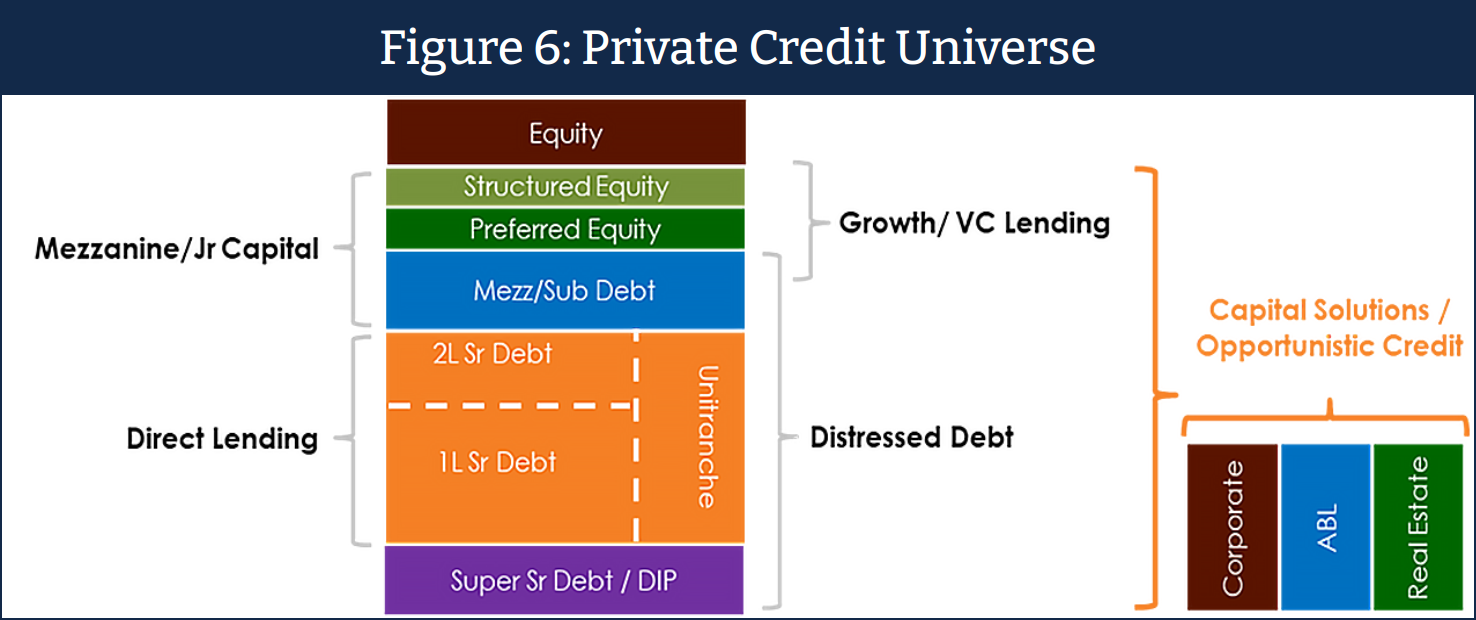

Finally, by offering borrowers more than a one-size-fits-all unitranche financing in the vein of its large, plain vanilla direct lending counterparts, flexible lenders can capture a complexity premium, with fully customized financing solutions taking many shapes (Figure 6). Moreover, with spreads compressed and competition high, lenders with flexibility to include junior debt securities as part of a comprehensive capital solution can differentiate themselves and generate higher blended returns, so long as they remain disciplined in terms of downside protection in their underwriting. Finally, private credit strategies can be differentiated from more commoditized direct lending by encompassing niche lending opportunities outside of traditional corporate lending that are increasingly filling voids left by commercial banks. ABL lending, in particular, can offer lenders access to high-quality non-corporate collateral ranging across both financial assets and hard assets, such as real estate, receivables, critical equipment, and legal claims.

About the authors: Javier Dyer is a Senior Managing Director and Co-Head of Opportunistic Investments at EnTrust Global. In addition, Mr. Dyer focuses on underwriting opportunistic credit situations, with an emphasis on private credit loans. Mr. Dyer joined the firm as a Senior Financial Analyst in August 2003. Before joining the firm, Mr. Dyer was a Credit Analyst in the Asset Management department at Atlantic Security Bank, where he was responsible for supervising portfolios of emerging market debt and U.S. high yield debt securities. He started his career as a Credit Analyst for the commercial lending arm of Credicorp Ltd., a U.S. listed financial conglomerate. Mr. Dyer holds an MBA in Finance from The Wharton School of the University of Pennsylvania, and a BS in Business Administration from Universidad de Lima, Peru.

Greta Ulvad is a Senior Vice President on EnTrust Global’s Opportunistic Investment Team. She is responsible for the sourcing, diligencing, and monitoring of investments across the capital structure in both private and public companies. Before joining the firm in 2016, Greta was an Associate in the Financial Restructuring Group at Milbank, Tweed, Hadley & McCloy LLP. She holds a JD from Vanderbilt University Law School and a BA in Psychology summa cum laude from Vanderbilt University.

Disclosures: PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. Statements or opinions reflecting predictions or perceived trends may be incorrect. Charts, tables and graphs contained in this document are not intended to be used to assist the reader in determining which securities to buy or sell or when to buy or sell securities. Targeted projections are HYPOTHETICAL and are not actual returns, profit forecasts or predictions. They are presented for illustrative purposes only and may only be achieved under certain conditions. There is no guarantee that these conditions will occur. This presentation does not represent all possible scenarios or outcomes and actual performance results may vary materially.

Endnotes:

1Source: Preqin, data as of December 2024.

2Source: Valuation Research Corporation.

3Source: KBRA, PitchBook LCD, Morgan Stanley Research.

4 Source: S&P; Morgan Stanley Research.