Benefits and Opportunities in Private Equity Co-Investing

By: Kristina Pierce, Mesirow

This article outlines how co-investing has emerged as a central strategy in private equity, offering institutional investors—including pension funds—enhanced portfolio control, the potential for improved returns through reduced fees, and deeper engagement with fund managers when pursued via a well-structured program.

Co-investment has become an increasingly prominent strategy within private equity, shaped by evolving macroeconomic conditions and the strategic objectives of both general partners (GPs) and limited partners (LPs). While co-investment can enhance portfolio diversification and returns, it demands access to high-quality GP networks and the expertise to evaluate and execute transactions efficiently.

The Rise in Co-Investment Activity

In recent years, GPs have increasingly turned to co-investment as a means of funding transactions, driven partly by extended fundraising cycles and higher interest rates.

The average fundraising timeline for GPs has grown by 30% over the past five years1, making it more difficult to secure target equity commitments while deploying a fund before it is fully raised. By involving current and prospective LPs in funding deals within their pipeline, GPs can begin constructing portfolios even as fundraising continues, effectively navigating the challenges posed by prolonged fundraising environments.

In addition, higher interest rates in the post-ZIRP era have made leverage a less attractive option to financing private equity transactions. When interest rates surged between 2022 and 2023, private equity firms faced challenges accessing debt markets and increasingly relied on equity for deal financing. In 2023, more than half of deals funded in the broadly syndicated loan (BSL) market had sponsors covering at least 50% of the overall deal value with equity2. Although this proportion declined in 20252, the significant role of equity from co-investors in deal structuring is likely to persist.

Benefits of Co-Investment to GPs and LPs

As the private equity industry continues to mature and evolve, co-investment is increasingly used as a tool by GPs and LPs to strengthen relationships and achieve certain goals for their investment portfolios.

Offering co-investment to LPs allows fund managers to pursue investments that require larger equity checks without reaching fund concentration limits, while also creating opportunities to develop a more strategic relationship with their limited partners. Having more touchpoints and regular dialogue with limited partners can also create more momentum for a manager’s primary fundraising efforts.

For LPs, co-investing provides certain advantages, including a greater level of discretion over private equity portfolios, the ability to form strategic relationships with GPs, and the opportunity to average down fees.

As an investor’s private equity program matures, co-investing enables LPs to concentrate their exposure with preferred managers or portfolio companies, enhancing strategic control over their portfolio.

Participating in co-investment processes also allows LPs to engage with their managers at deeper level, providing an “inside look” at how GPs prosecute deals, as well as the quality of their teams, the thoroughness of their diligence process, and how they utilize their operating resources and networks. These insights help LPs discern a GP’s quality and competitive advantages.

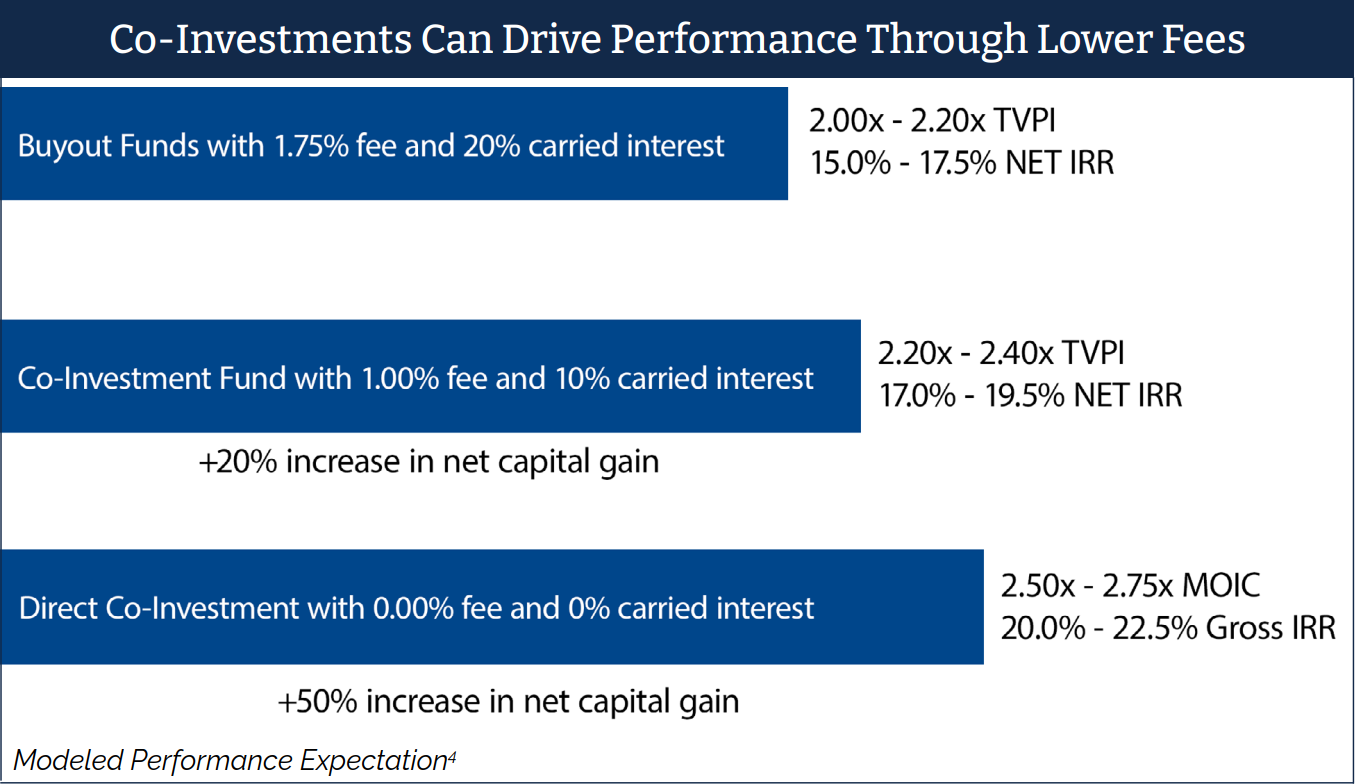

Finally, one of the most compelling reasons LPs seek co-investment is that they are generally offered at little or no attached economics, including the absence or reduction of management fees and carried interest, which allows LPs to lower the overall cost of their private equity portfolios and achieve higher risk-adjusted returns.

Given these benefits, many LPs now allocate 15% – 30% of their total private investment portfolios to co-investment opportunities3.

All Co-Investors Are Not Created Equal

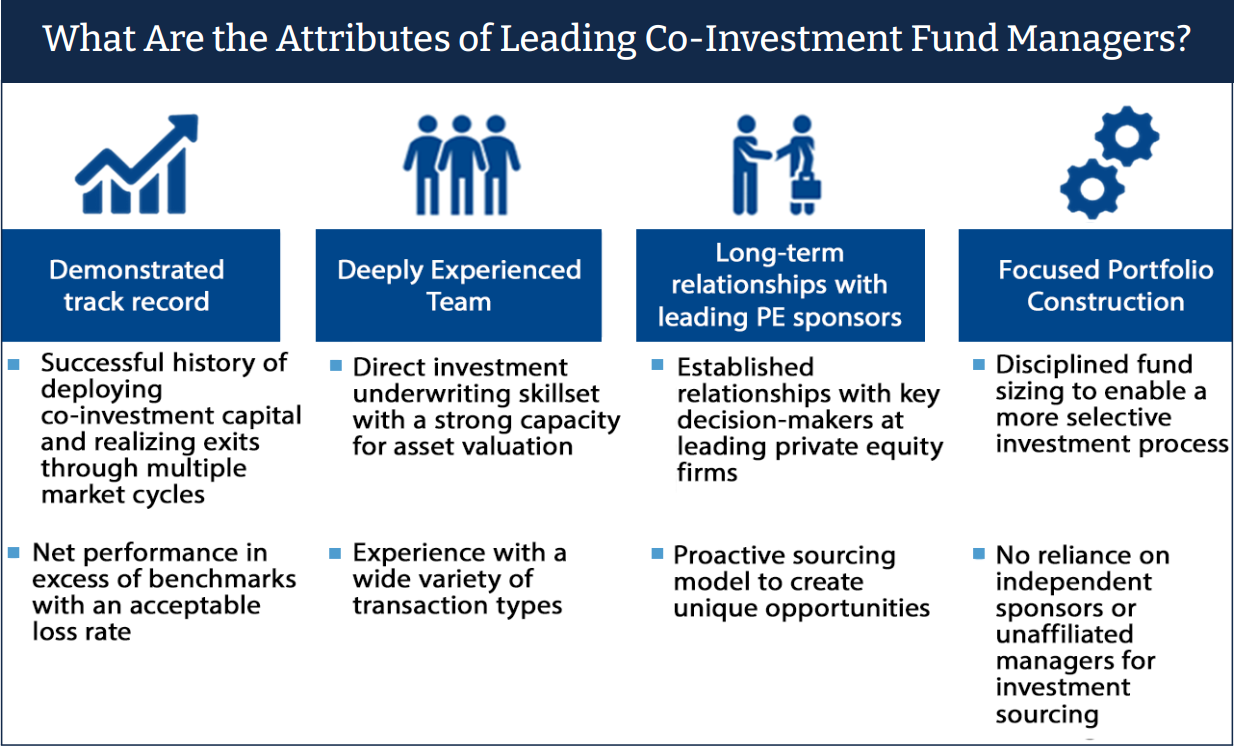

A successful co-investor demonstrates a combination of strategic resources, robust networks, and specialized expertise. Investors must assess whether they possess the internal capabilities — such as experienced teams and relevant industry connections — to source, evaluate, and execute co-investment opportunities independently, or if partnering with a dedicated co-investment fund would be more effective.

Building a high-quality, diversified co-investment portfolio requires cultivating strong relationships with GPs who have proven value creation strategies and sector expertise. Effective co-investors also excel in due diligence, leveraging pattern recognition and analytical skills to prioritize deal flow and assess opportunities across multiple dimensions, including strategic fit, market risks, financial trends, and underwriting assumptions.

Furthermore, co-investors distinguish themselves by being responsive to GP timelines and processes, and by adding value through introductions and strategic support to portfolio companies. As competition for co-investment allocations increases, standing out in the eyes of GPs is essential — not only for access to deals, but also for building enduring, mutually beneficial partnerships.

Conclusion

Private equity co-investing offers significant advantages for both GPs and LPs. For GPs, it provides a flexible funding mechanism and strengthens relationships with investors. For LPs, co-investment delivers greater control, transparency, and the potential for enhanced returns through reduced fees. However, success in co-investing requires robust sourcing networks, strong diligence capabilities, and the ability to align with GP processes. As the market continues to evolve, co-investment is expected to remain a valuable tool for sophisticated investors seeking to optimize their private equity portfolios.

About the author: Kristina Pierce is a Senior Managing Director at Mesirow Private Equity and a member of the firm’s Investment Committee. Prior to joining the firm in 2007, Kristina was an Investment Banking Analyst in the mergers and acquisitions and global industrials groups at UBS Investment Bank in Chicago. Ms. Pierce has 20 years of expertise in investment management and capital markets.

An avid supporter of civic engagement, Kristina is involved with Private Equity Women Investor Network (PEWIN) and serves on the Board of Directors of Cristo Rey Jesuit High School.

Kristina earned a Bachelor of Business Administration from the University of Notre Dame, where she has been a guest lecturer, and is a CFA® charterholder.

Endnotes:

1 Source: PitchBook.

2 Source: PitchBook LCD.

3 Private Funds CFO, Fees and Expenses Survey, Published in association with: Troutman Pepper, Withum and Vistra • October/November 2024.

Model reflects cost of different fee structures; assumes buyouts underwritten to gross MOIC of 2.50x to 2.75x over five-year holding period. Standard terms for Buyout Fund modeled with 1.75% management fee on committed capital during investment period, switching to remaining cost thereafter, and 20% carried interest with 8% preferred return and 100% GP-catchup. Standard terms for a Co-investment Fund reflect a 10% carried interest with 8% preferred return and 100% GP-catchup, and a 13-year average annualized management fee of 82 bps. Assumes no underlying management fees or carried interest but does pay a one-time transaction fee of 1% on invested capital. Pacing for Buyout and Co-Investment Funds assumes weighted 5-year average holding period. There is no assurance that actual results will meet assumptions.