Beyond U.S. Exceptionalism

By: Don Dimitrievich, Nuveen

In today’s volatile markets, pension funds can strengthen portfolio resilience by diversifying alternative credit allocations across geographies and asset classes, reducing overreliance on any single market. Nuveen’s research highlights how energy infrastructure credit — supported by powerful structural tailwinds including AI-driven power demand, domestic manufacturing and electrification — can offer pension investors stable, risk-adjusted income even in uncertain times.

Concerns are growing over economic activity, political tension, and policy uncertainty in the U.S., creating a challenging investment environment. Headlines throughout 2025 and so far in 2026 underlined this uneasiness; foreign investors were reportedly leaving U.S. markets in droves amid currency volatility and tariff-driven fears, possibly spelling the end of U.S. exceptionalism as we know it. Adding to these doubts is the specter of an increasingly deglobalized world.

In this climate, separating rhetoric from reality is crucial. In our opinion, the world may be changing, but global private credit — whether corporate or asset-backed — remains an attractive opportunity set for those seeking diversified sources of stable income in an unstable time. Institutional investors can build resilience with alternative credit by diversifying exposure across a range of asset classes and across the U.S. and Europe.

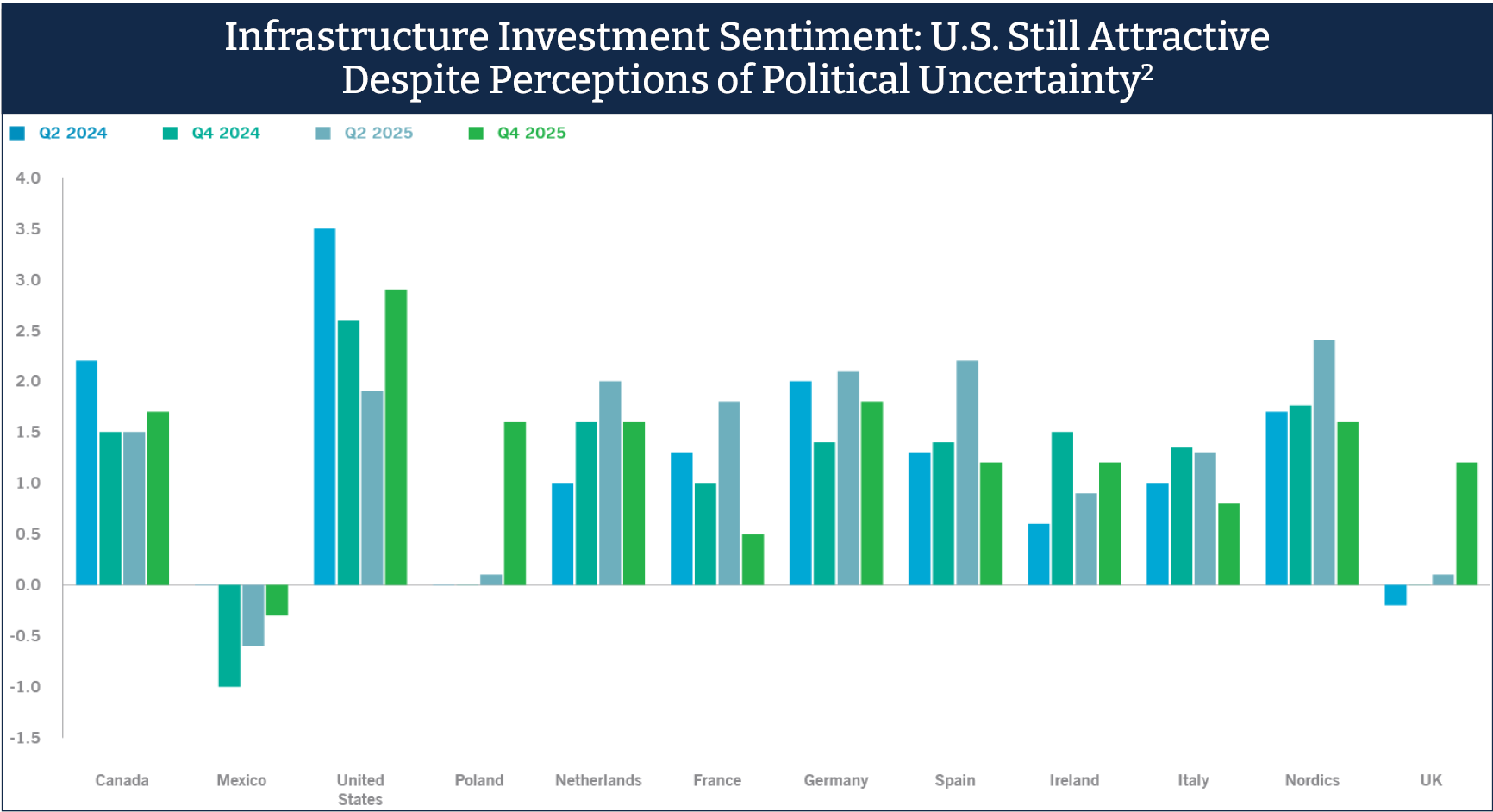

U.S. Remains a Rich Source of Opportunity Despite New Risks

Despite the uncertainty, the U.S. economy has demonstrated its ability to withstand shocks and beat pessimistic forecasts. Corporate earnings remain robust, and default rates for U.S. credit, especially among higher-rated borrowers, remain overwhelmingly stable.1 Despite the U.S. dollar weakening through 2025 and into 2026, it continues to anchor international portfolios, providing depth and liquidity that few global markets can match.

In this environment, we believe U.S.-based credit continues to play an important source of portfolio diversification. Investors are drawn by its strong fundamentals, attractive risk-adjusted yields, and proven resilience.

While issues such as the First Brands’ and Tricolor bankruptcies have cast a shadow over private credit, industry experts and allocators stress that these incidents remain isolated, driven by inadequate diligence and lax underwriting, rather than broader economic malaise. Disciplined managers continue to demonstrate the importance of robust due diligence in an environment rich with opportunity but not without risk.

Europe Offers Unique Risk Diversification Exposure

While the U.S. remains attractive, the universe for alternative credit is broader than one market. We’re seeing Europe offering pockets of long-term value, especially in non-cyclical sectors and upper middle market lending. The stronger euro, likely in response to the weaker U.S. dollar, exemplifies the benefits of geographic diversification in times of global uncertainty.

According to a recent survey of asset managers globally, 37% of respondents identified European direct lending as having the most growth potential over the next five years.3 Opportunities in Europe reflect the continent’s geopolitics. A continued focus on energy infrastructure for both renewable energy and energy security, for example, demonstrates how structural changes are driving compelling investments. These same factors are acting as catalysts for investment grade private credit.

Energy Infrastructure Credit

From our perspective, infrastructure debt as an asset class continues to present attractive investment opportunities for investors. It is supported by rapid power demand growth from AI datacenters, onshoring of manufacturing, and electrification.

In the U.S., private infrastructure debt investments across energy, power, and digitalization steadily climbed from approximately $120 billion in 2021 to nearly $350 billion in 2025. This is not only expected to increase, but there is over $600 billion of debt maturing before the end of 2030.4 Our research explains why we see energy efficiency, community solar, domestic manufacturing, and U.S. liquified natural gas offering attractive risk-adjusted opportunities in this environment. These energy and power investment themes address critical supply-demand imbalances that will likely persist for the next decade and are all supported by government policy.

About the author: Don Dimitrievich, is a Senior Managing Director and Portfolio Manager for Energy Infrastructure Credit at Nuveen, where he leads investment strategy, oversees portfolio management and chairs the Investment Committee for the EPIC funds and EIC platform.

Don brings over 25 years of investment experience to his role. Prior to joining Nuveen in 2022, he was Head of Energy & Power and a Partner at HPS Investment Partners, where he founded and led the energy and power investment vertical. Previously, he served as a Managing Director at Citi Credit Opportunities, overseeing power, renewables and energy investments. Don began his career as an attorney at Skadden, Arps, Slate, Meagher & Flom LLP, focusing on energy and power M&A.

Don holds a JD with Great Distinction from McGill University and a chemical engineering degree with Great Honors from Queen’s University.

Disclosures: This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial advisors. Financial professionals should independently evaluate the risks associated with products or services and exercise independent judgment with respect to their clients.

Past performance is no guarantee of future results. All investments carry a certain degree of risk, including the possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Certain products and services may not be available to all entities or persons. There is no guarantee that investment objectives will be achieved.

Nuveen, LLC provides investment solutions through its investment specialists.

5329303

Endnotes:

1. S&P Global “Default, Transition, and Recovery: Regional Divergences Should Keep The Global Default Rate Steady Through September” dated 26 Nov 2025.

2. Alvarez & Marsal (Q4 2025): Infrastructure Pulse – North America and Europe. Chart based on respondents answering “What is your outlook for the attractiveness of, and opportunities for, your fund(s) infrastructure investment in the following countries in the next quarter? (-5: extremely unfavourable, 0: neutral, 5: extremely favourable)”

3. Mercer “Private Markets in Motion: Private debt Taking the pulse of global asset managers” as of July 2025.

4. Infralogic (Accessed 24 Feb 2026).