Farmland: Real Estate at Its Core

By: Clint Leman, US Agriculture

Leased U.S. farmland is a pure form of real estate that delivers stable income, long-term appreciation, and strong inflation sensitivity, while being driven by enduring demand for food, fuel, and fiber rather than economic cycles. It highlights farmland’s structural advantages over traditional commercial real estate—including low leverage, minimal depreciation, productivity-driven growth, and shrinking land supply.

Institutional investors have long relied on real estate for income, diversification, and inflation protection. But with higher interest rates and structural changes reshaping office, retail, and multifamily, many are reconsidering traditional exposures. One compelling but underutilized alternative is leased U.S. farmland, which provides many of real estate’s strengths while offering distinct advantages in return stability, inflation sensitivity, and independence from broader economic cycles.

Farmland Is Real Estate

Real estate consists of land and any fixed improvements leased to tenants in exchange for rent. Leased cropland is one of the purest forms of real estate, as its underlying value is almost entirely attributable to land—a finite, tangible, non-depreciable asset.

Like commercial real estate (CRE), farmland produces recurring income and long-term appreciation. But unlike CRE, it is tied to global demand for food, fuel, and fiber, which remain essential regardless of economic cycles.

Where Farmland’s Value Comes From

Agricultural Output as a Stable Driver

Farmland derives value from agricultural production, while CRE depends more on economic activity, interest rates, and labor markets. Both asset types benefit from capital improvements, though the nature differs: CRE owners invest in tenant amenities, while farmland owners typically invest in yield-enhancing improvements like drain tile, irrigation, and grain storage.

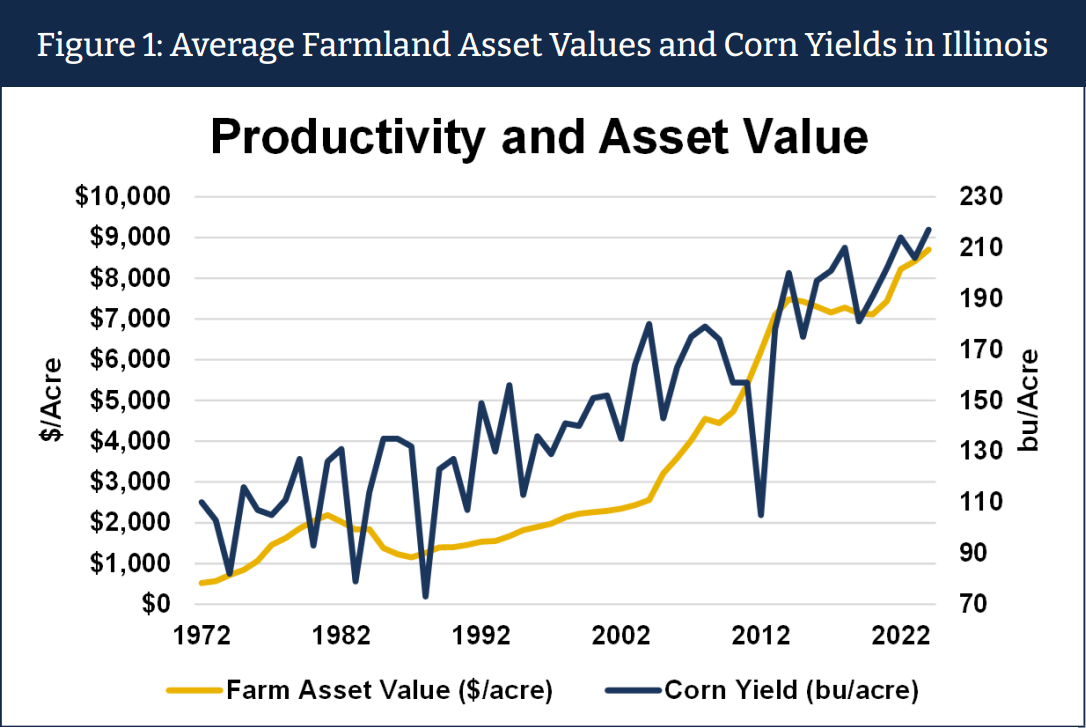

Productivity Growth: A Unique Long-Term Tailwind

Farmland has benefited from continuous yield improvements, much of which occurs without proportional capital investment from the landowner. Advances in seed genetics, equipment, and agronomy steadily increase productivity.

Since WWII, U.S. crop productivity has increased roughly 2% per year. This productivity growth enhances both income and asset value.

Structural Advantages of Leased Cropland

Lower Leverage and Better Behavior During Inflationary Periods

CRE commonly employs 30–140% leverage. By contrast, the agricultural sector uses roughly 15% leverage, reducing refinancing and rate-sensitivity risks.

Leased cropland has historically exhibited stronger correlation to inflation than CRE. In inflationary environments, farmland historically benefits from higher commodity prices and rising cash rents.

Minimal Depreciation and Obsolescence

Annual cropland consists almost entirely of non-depreciable land. CRE and permanent cropland contain significant long-lived improvements, making them more vulnerable to physical obsolescence due to changes in demand.

Farmland typically requires <1% annual capex, compared to ~2% for CRE. Additionally, tenant demand for annual cropland tends to be competitive and renewable each season, resulting in near-zero vacancy.

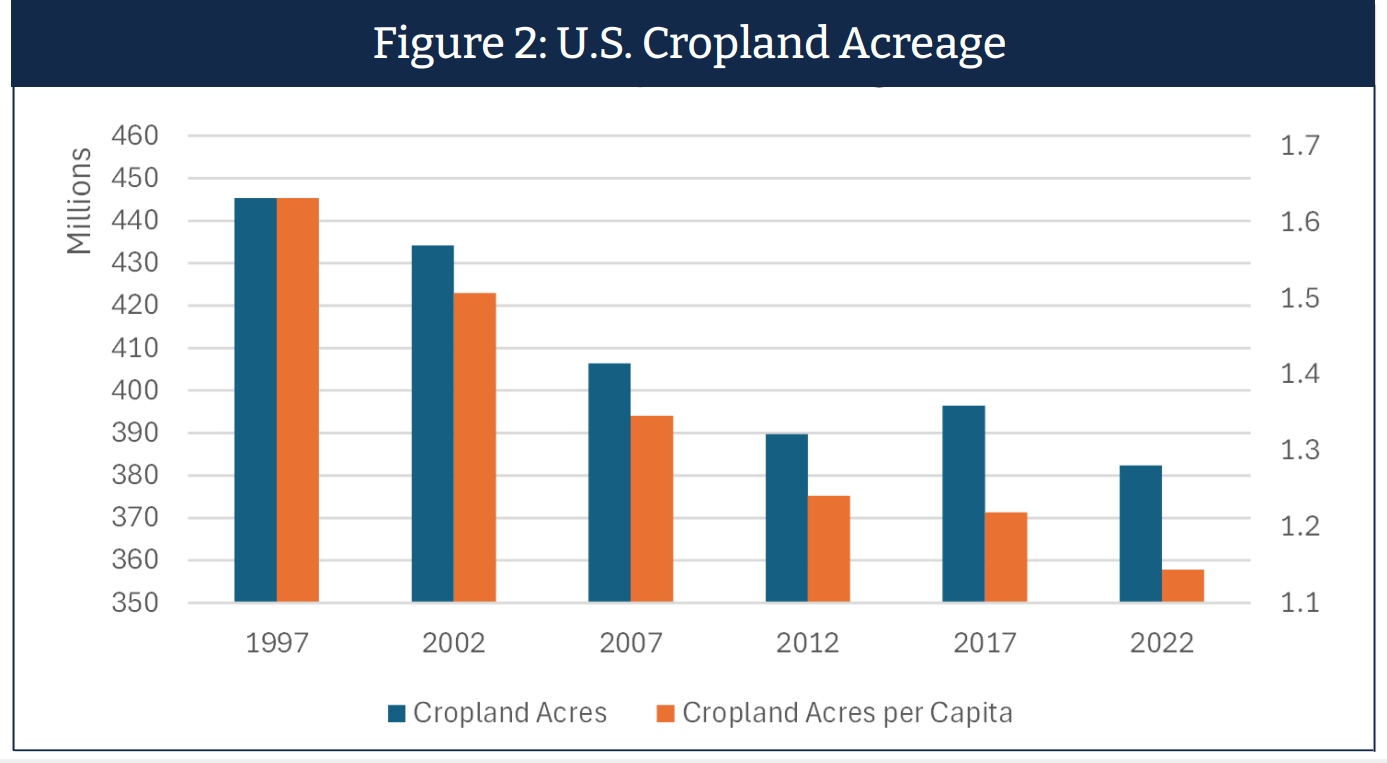

Urbanization Reduces Supply

Urban expansion has steadily reduced U.S. farmland for decades as seen in Figure 2. As farmland becomes scarcer, remaining productive land should become increasingly more valuable.

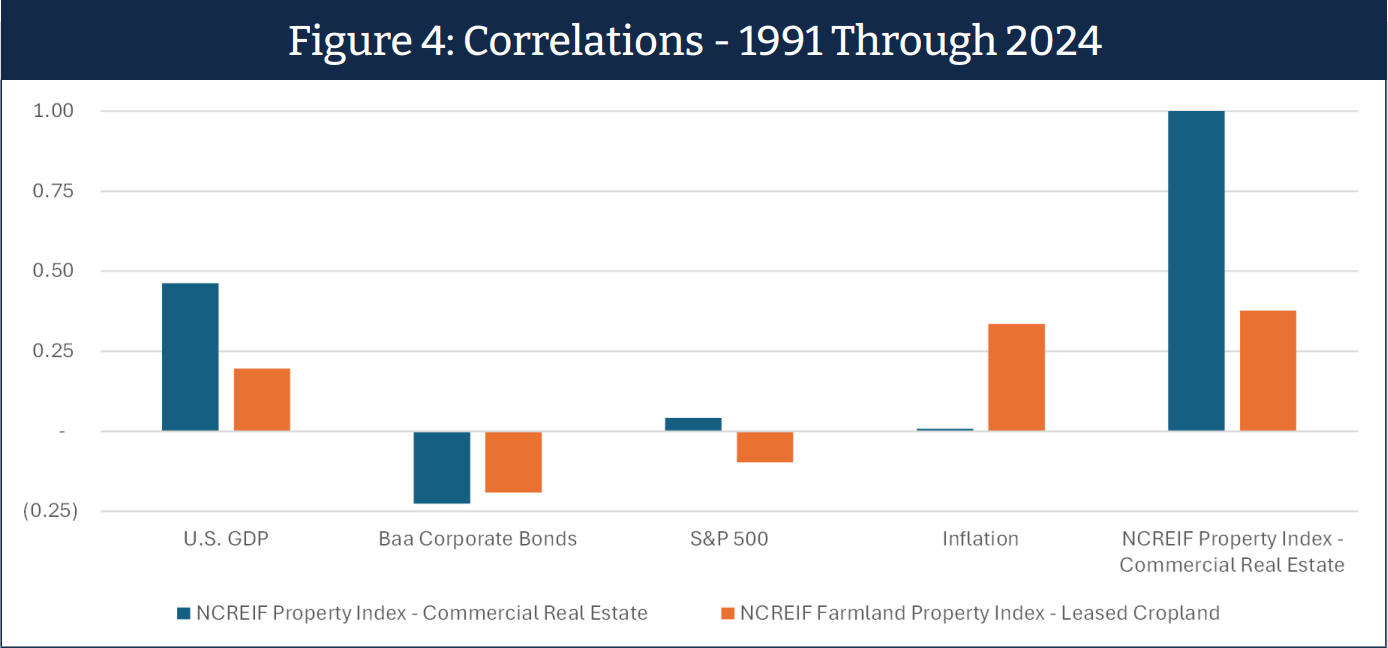

Return Characteristics: Stability, Diversification, and Inflation Protection

Since the NCREIF Farmland Property Index began in 1991, leased cropland has demonstrated clear performance differences compared to the NCREIF Property Index (CRE). Leased cropland has:

- Outperformed CRE across multiple time periods (see Figure 3).

- Never posted a negative annual return.

- Experienced lower correlations to GDP, stocks, and bonds, offering stronger diversification (see Figure 4).

- Experienced higher correlation to inflation, suggesting it is a stronger hedge against inflation (see Figure 4).

Adding farmland to a CRE allocation can improve risk-adjusted returns.

Conclusion

Amid elevated interest rates and structural shifts in traditional real estate markets, leased U.S. cropland offers a compelling alternative to CRE. Its fundamentals — tangible land, resilient income, long-term appreciation, low volatility, and inflation protection — position it as an asset class with the ability to enhance portfolio stability and increase diversification.

Click here to download the full-length analysis from US Agriculture, LLC’s website.

About the author: Clint Leman, CFA, is the Director of Portfolio Management responsible for managing select client portfolios, overseeing investment analysis, and performing all other aspects of portfolio management and is a member of USAG’s Board of Managers. Prior to joining USAG, Clint was an Equity Analyst and Portfolio Manager at Martin Capital Management, a value-oriented, investment advisor. Clint earned a B.S. in Business and Economics, with a concentration in Finance, from Indiana University South Bend. Clint is a CFA® charterholder, and a member of the CFA Society of Indianapolis. Clint grew up on a pork and grain farm in northwest Indiana. Clint is a member of the Pension Real Estate Association and the National Council of Real Estate Investment Fiduciaries (“NCREIF”).

Disclosures: Information contained herein is as of the date hereof or as of the date(s) noted, as applicable. Information may be based, in part, on information from third parties believed to be reliable or assumptions that later prove to be invalid. Information contained herein is not intended to be relied upon as the basis for an investment decision. US Agriculture, LLC disclaims any obligation to update this presentation. No warranty, express or implied, is made by US Agriculture as to the accuracy or completeness of the information contained herein. The contents are not to be construed as legal, business, or tax advice.

Certain information contained herein may constitute “forward looking statements”. Actual results may differ materially from those contemplated in such statements.

Registration as an Investment Advisor does not imply any level of skill or training.

Historical farmland value is no guarantee of future value.

Endnotes:

Figure Sources:

1USDA Quick Stats.

2USDA Quick Stats (Cropland Acres); U.S. Census Bureau (U.S. Population); USAgriculture Analysis.

3https://user.ncreif.org/data-products/ncreif-query-tool/ (NCREIF Property Index - Commercial Real Estate and NCREIF Farmland Property Index – Leased Cropland); USAgriculture analysis.

4https://user.ncreif.org/data-products/ncreif-query-tool/ (NCREIF Property Index - Commercial Real Estate and NCREIF Farmland Property Index – Leased Cropland); https://pages.stern.nyu.edu/~adamodar/New_Home_Page/data.html (S&P 500, Baa Corporate Bonds); International Monetary Fund (U.S. GDP); U.S. Bureau of Labor Statistics (Inflation); USAgriculture analysis.

5As of December 31, 2024, there were over 760 leased properties within the NCREIF Farmland Property Index (“NFI”) accounting for approximately $11.4 billion of real estate value. Of that amount, approximately 85% was annual cropland. The NCREIF Property Index (“NPI”) has been used to represent commercial real estate (“CRE”). The NPI began in the fourth quarter of 1977 and is comprised exclusively of operating properties. The NPI includes industrial properties, apartments, offices, retail properties, and hotels. As of December 31, 2024, NPI was comprised of over 10,500 properties worth over $810 billion. For additional information on the NFI and the NPI visit https://ncreif.org/.