Mastering Governance: Who Should Make Decisions About Manager Selection?

By: Julie Becker and Katie Comstock, Aon

This article highlights how public funds can evaluate the advantages and considerations of delegating manager selection to staff or an external party versus retaining the responsibility within the board or investment committee.

Public pension trustees have a crucial role in the oversight of plan assets, a role that requires a great deal of integrity, dedication, and access to resources and tools. One such tool is the delegation of investment manager selection, a practice increasingly under discussion among investment committees and boards of many public funds. The goal is to establish an effective and efficient selection process that gives the board more time to focus on high-level policy matters, while giving staff and/or external advisors the flexibility to make timely investment decisions. However, effective delegation must be accompanied by robust reporting and monitoring frameworks so that the board — the ultimate fiduciary — can fulfill its fiduciary duty to safeguard and invest plan assets. Aon Investments’ research of the 50 largest public pension funds in the U.S. found that roughly half of those plans employ a form of delegation.

Delegation Best Practices

The duty of prudence not only permits but also expects boards to delegate certain responsibilities. Delegation is a fundamental aspect of sound governance that allows for more efficient and effective decision-making. It involves assigning specific responsibilities to individuals or groups with the expertise to handle them. For public funds, this often means delegating certain investment decisions to qualified agents, which could be staff and/or advisors, while maintaining overall oversight. The delegation process should be clearly documented, with well-defined roles and responsibilities, to ensure accountability and transparency. The board’s “sign-off” on the process is crucial, ensuring that all parties understand their duties and the resources available to them. A structured approach helps ensure that delegation enhances, rather than diminishes, the board’s ability to act in the best interests of plan participants and beneficiaries.

Necessary Elements for Responsible Delegation

To ensure prudent delegation, several elements must be in place:

- Sufficient resources to implement effectively

- Appropriate and clear parameters precisely defining what is being delegated

- Robust process for manager selection

- Monitoring standards and expectations

- Board action to approve the delegation and monitor it

Benefits and Considerations of Delegation

Delegation offers several benefits, including more efficient and expeditious investment decisions, greater flexibility for experts to complete their duties, and more time for the board to focus on higher priority items such as asset allocation and policy decisions. If implemented correctly, delegation can enhance fiduciary oversight and risk management by holding delegated activities to specific processes and standards, including reporting requirements. However, delegation is not without risk. Reduced participation from the delegating body (board or investment committee) can lead to complacency in oversight and monitoring. To mitigate these risks, it is essential to set appropriate parameters and procedures, conduct regular reviews, and ensure transparency and concurrence from all parties involved.

Prevalence of Delegation

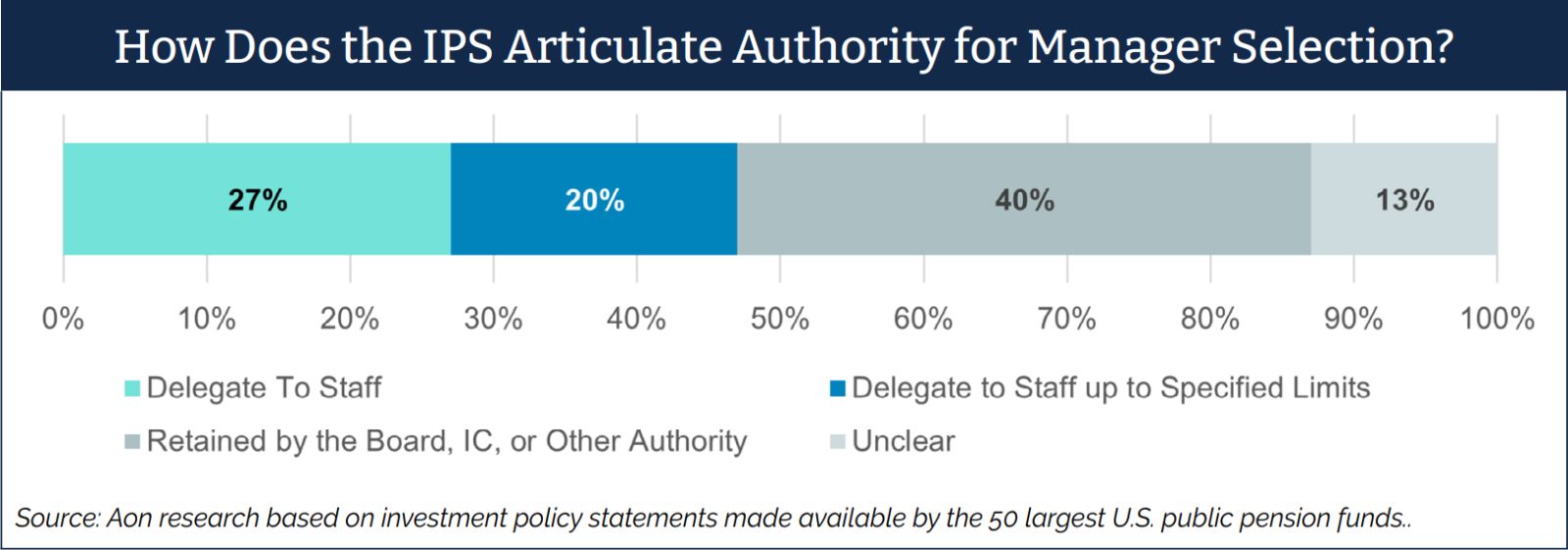

Aon Investments surveyed the investment policy statements of the 50 largest public pension funds in the U.S. for delegation of manager selection.1 Our study found a roughly even split between plans that delegate some or all manager selection to staff versus plans that retain manager selection at the board, investment committee, or other authority level. Of those where manager selection is delegated to staff, a significant portion specified size limits for the delegation, usually a limit as a fixed dollar amount or percentage of plan assets. The following exhibit shows the detailed results from our study.

It is important to note that our study was on very large plans with assets ranging from about $25bn to over $500bn, which often have large internal investment teams, and thus tend to be more likely to have the resources and staff with the skills to select managers. For plans without large staff, delegation to staff may be less common; if delegation exists, it is likely more common for them to fully or partially delegate to third-party advisors. A common delegation model is to give discretion to a third-party advisor for a specific private market asset class, such as private equity, which can be very resource intensive. Some plans use an Outsourced Chief Investment Officer (OCIO), which is when an outside firm is delegated discretionary responsibility for all investment manager selection, among other operational duties (such as raising liquidity and rebalancing).

Conclusion

There is no one-size-fits-all solution, and the level of delegation largely depends on the comfort level with the delegating body and the processes and resources in place. Aon recommends selecting a model that works best for all constituents involved, ensuring transparency and buy-in on processes and procedures. An approach with clearly defined processes and parameters, and robust reporting requirements, can lead to a successful delegation model.

About the authors: Julie Becker is a partner and leader of Aon’s Fiduciary Services practice at Aon Consulting, Inc. In this role, she is responsible for providing fiduciary and governance advisory services to various public, corporate, and endowment and foundation institutional decision makers.

Katie Comstock is a partner and leads public sector solutions at Aon Investments USA. Katie consults to state and local public entities on governance, investment policy, asset-liability analysis, asset allocation, risk budgeting, and portfolio structure, helping public sector organizations achieve their investment objectives.

Disclosures: This article is a general communication being provided for informational purposes only. The opinions expressed represent the current, good-faith views of the author(s) at the time of publication. It is not designed to be investment advice or a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. Any forward-looking statements, estimates, and certain information contained herein, are based upon research and other sources that are subject to change. The information provided relates to Aon Investments USA Inc. (“Aon Investments”) and Aon Consulting, Inc. (“ACI”). Aon Investments is wholly owned by ACI, an indirect subsidiary of its ultimate parent, Aon plc. Aon plc is a diversified professional services company, and such services are provided through various subsidiaries and/or affiliates. Investment advice and investment consulting services provided by Aon Investments. Non-investment consulting services provided by ACI.

Endnotes:

1. Source: Aon Research. Data provided for informational purposes only, and should not be considered investment advice. The study includes the 50 largest U.S. public pension funds, in which five of those funds were excluded from our study because they either did not have an investment policy statement at the time of the study (August 2025) or we could not get a copy of the investment policy statement. The charts, assumptions and any commentary herein are considered proprietary opinions of Aon based on the expertise of Aon’s Manager Research Team along with readily available economic and market information as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.