Discount to Fair Value: How to Strengthen Pension Portfolio Resilience through Tech Secondaries

By: Artea Global

This article explains how pension funds can access best-in-class, high-growth, late-stage private technology companies at significant discounts to public market valuations through a small-ticket secondaries manager — and why a disciplined underwriting framework makes this strategy particularly well-suited to pension funds’ long-term, capital-preservation mandates.

In early 2026, roughly half of publicly traded software companies tracked by institutional analysts reached three-year valuation lows as fears of AI agents displacing enterprise software triggered indiscriminate selling with names such as ServiceNow, HubSpot, and Adobe falling between 20% and 60% from recent highs. Yet a select group of late-stage private technology companies, those with genuine AI tailwinds, non-discretionary revenue, and defensible data moats, continued to outgrow their public peers and have remained largely insulated from selling pressure.

Exposure to many of these companies is attainable through the secondary markets at meaningful discounts to public comparables. By assembling stakes from small-ticket sellers such as early employees, end-of-life funds, and family offices, allocators can access high quality technology businesses at entry valuations typically unavailable in primary rounds or public markets. Applied with discipline to a carefully curated target list, this represents an asset class that pension investment committees should examine closely.

Structurally Growing Market with Motivated Sellers

The VC secondary market has expanded from approximately $60 billion in annual deal volume in 2020 to over $140 billion in 2023, a compound annual growth rate of roughly 30%, with direct secondaries in private technology expected to remain among the fastest-growing segments over the next decade.

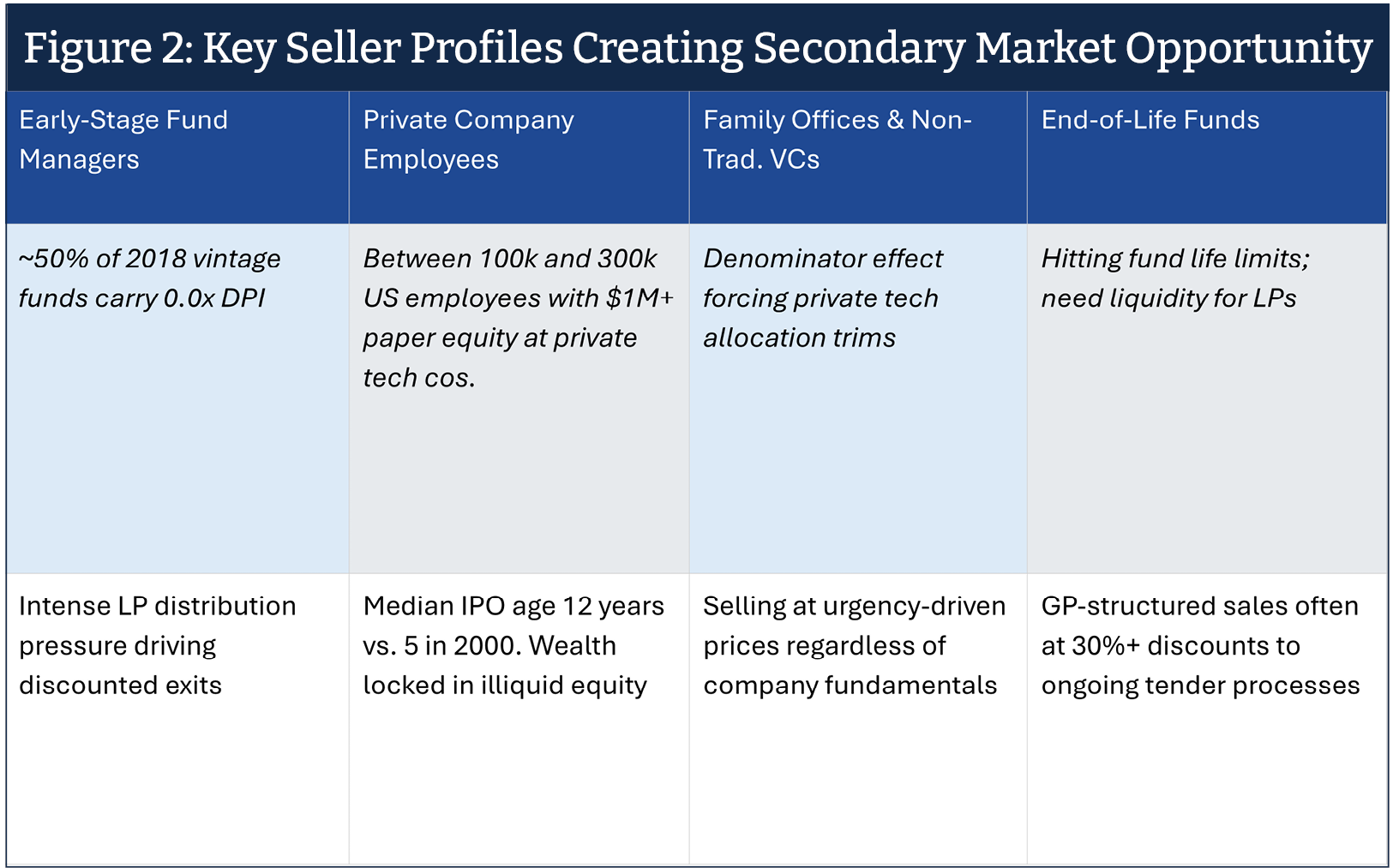

The supply of motivated sellers is both large and durable. Approximately 50% of 2018 vintage funds reported 0.0x DPI, placing early-stage managers under increasing pressure to generate distributions. At the same time, an estimated 100,000 to 300,000 employees at private technology companies hold over $1 million in paper equity, concentrated in a relatively small number of late-stage companies, many of which are opting to remain private longer. With the median IPO timeline extending to approximately 12 years (versus 5 in 2000), much of this paper wealth may remain illiquid for prolonged periods. Meanwhile family offices and non-traditional investors facing denominator constraints have also been active sellers. Across these cohorts, pricing is often driven by liquidity needs rather than intrinsic value, thereby sustaining a consistent supply of secondary opportunities.

The Governance Case: Why Secondaries Suit Pension Mandates

A well-constructed late-stage technology secondary program is distinguished from higher-risk technology allocations by three governance-positive attributes:

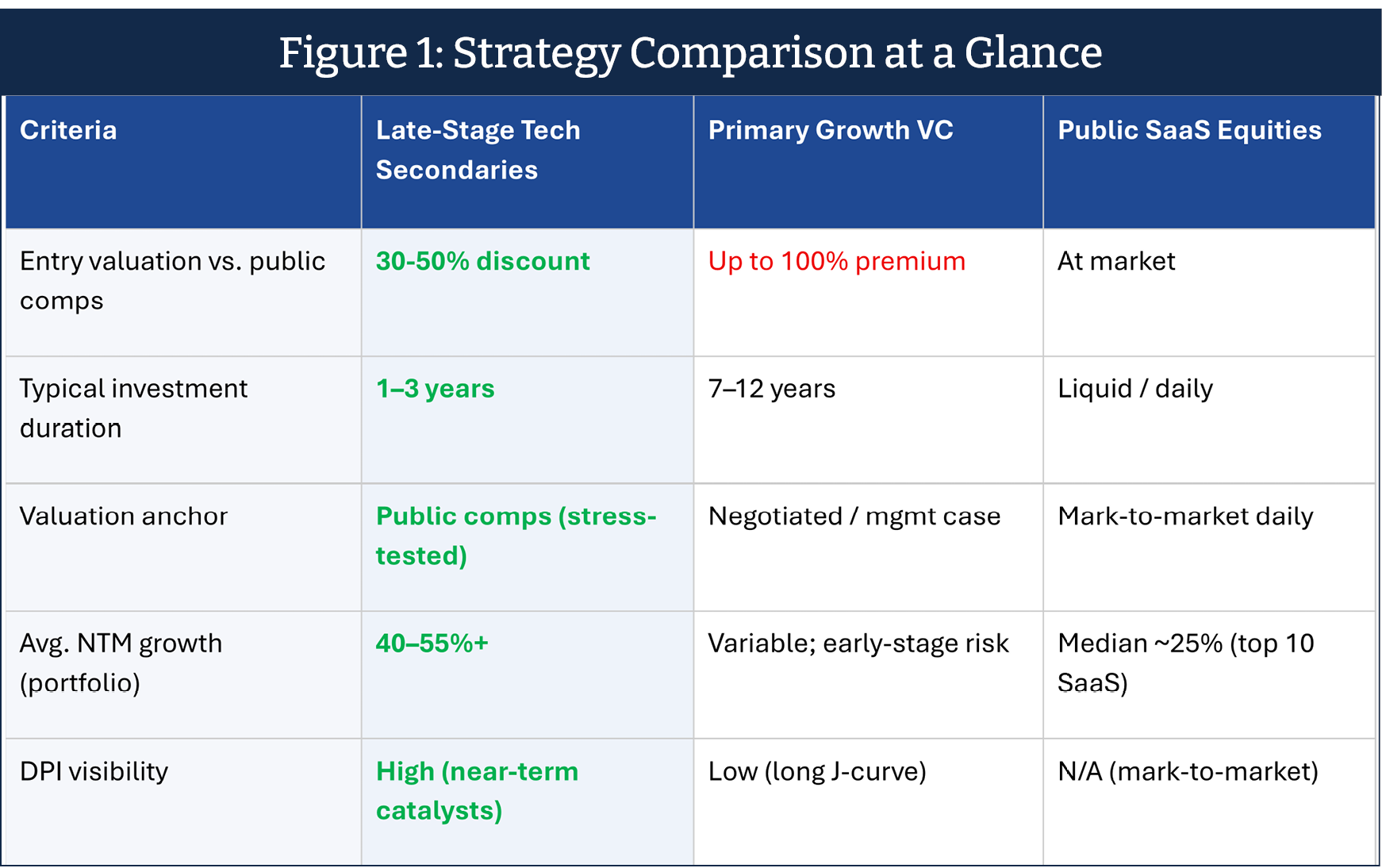

- Valuation discipline anchored to public markets. Managers can benchmark entry pricing against public comparables and underwrite to conservative scenarios, including downside cases informed by dislocations such as the 2022–23 sell-off. Small-ticket managers can access materially lower entry points levels than large block transactions by sourcing directly from motivated sellers and applying appropriate illiquidity discounts.

- Superior liquidity visibility versus traditional VCs. Late-stage assets benefit from identifiable near-term exit catalysts, including IPOs, M&A processes, and tender programs, enabling more credible DPI forecasting and alignment with actuarial cash flow planning. Unlike 10-year blind-pool VC structures, investors retain the flexibility to monetize positions through the secondary market as needed.

- Concentration management. Position sizing limits of 10–15% per name, combined with deliberate sector diversification, can reduce idiosyncratic risk to levels comparable to disciplined public equity portfolios.

Portfolio Construction and the Margin of Safety

Not all technology companies are equally resilient to AI disruption. Cybersecurity, data infrastructure, and vertical SaaS have in many cases demonstrated continued revenue acceleration during the sell-off while segments such as marketing technology, generic enterprise SaaS, and certain DevOps tooling, have experienced meaningful (e.g. >30%) valuation compression. Any secondary program should explicitly incorporate screening for AI resilience.

Pricing remains a crucial source of return. Small-ticket transactions, typically $15 million or less, often clear at entry multiples between 30% and 50% below public market comparables. This pricing advantage is largely unavailable to larger funds focused on LP stake or big block transactions. At the same time, primary investors in select AI companies have paid significant premiums to public benchmarks, reinforcing the relative attractiveness of disciplined small-ticket secondary entry points.

A Call to Examine the Allocation

The lesson from 2022–23 and early 2026 is not that pension funds should avoid technology. It is how you access technology that determines whether volatility is a risk or an opportunity. CIOs and trustees should assess whether current investment policy statements accommodate small-ticket direct secondary strategies, distinct from both primary venture capital and large-format GP/LP secondary funds. Where such flexibility does not exist, establishing a dedicated allocation within the alternatives portfolio, sized appropriately, warrants consideration.

In a market where growth is rewarded and motivated sellers exchange liquidity for discounts, the best positioned pension funds are those that combine disciplined entry pricing with the conviction to hold through short-term noise. That is not a new principle, it reflects a core tenet of long-term pension investing.

About Artea Global:

Artea Global is an institutional direct secondaries fund focused on acquiring stakes in best-in-class late-stage technology companies. Founded in 2022, the firm targets small, highly idiosyncratic transactions sourced from motivated sellers, including early employees, end-of-life venture funds, and family offices. This strategy enables Artea to provide its LPs with access to high-quality private technology businesses that are outperforming their public peers, at entry valuations typically unavailable through primary financings or large-format secondary funds.

Disclosures: Sources: Industry Ventures VC Secondary Market Research; Cambridge Associates Private Investment Benchmark Statistics; Artea Global Analysis. This article is for informational purposes only and does not constitute investment advice.