Reframing Infrastructure Investing: A Fixed-Income–Like Approach for Public Pensions

By: Jason McGaugh, Sustainability Partners

When evaluated through a cash flow lens, usage-based essential infrastructure looks a lot like fixed income — with stable, contract-supported revenue, long asset duration, and built-in inflation escalators. Here's how public pensions can put that to work.

Public pension funds face a persistent challenge: generating stable, long-duration returns while protecting portfolios from inflation and downside risk. As traditional fixed income struggles to meet these objectives in a volatile rate environment, many institutions are expanding allocations to Real Assets and Inflation Protection strategies.

Within this shift, essential infrastructure presents a compelling yet often underutilized opportunity. When viewed through a cash-flow lens, these assets share many characteristics with fixed income, while offering additional benefits tied to essential service demand, inflation resilience, and asset-level control.

Usage-based essential infrastructure investing resembles fixed income in function: stable, contract-supported cash flows tied to essential services, but with additional asset-level controls and an illiquidity premium, which can improve long-term resilience for pension portfolios. Structured correctly, usage-based payment structures can mimic fixed income cash flows - stable and predictable. Most essential infrastructure asset types can be structured to incorporate this concept.

We start with a clear framework for assessing critical infrastructure opportunities through a fixed income lens - focusing on asset resilience, cash flow stability, and long-term risk mitigation for public pension portfolios.

Similarities between Usage-based Essential Infrastructure and Traditional

Fixed Income:

Coupon Payments vs. Contracted/Tariff-Based Cash Flows – Both are designed to deliver predictable, steady cash flows; infrastructure cash flows are structured as recurring payments tied to asset operation plus customer usage while fixed income is generally a scheduled coupon plus principal payment. Both rely on structures that reduce downside risk and improve payment certainty; infrastructure has more “hands-on” control points than traditional fixed-income instruments.

Duration Matching: Liability-Driven Investing vs. Long Asset Life – Both can be used in liability-driven investment-style roles — stable cash flow to meet long-term obligations. Fixed-income maturities are explicit (10/20/30 yrs), whereas with essential infrastructure investments, assets and contract duration naturally match pension horizons (20-50 year asset life); and if structured correctly, can be characteristic of a perpetual cycle of capital deployment and long-term cash flow.

Inflation Protection: TIPS/CPI Linkage vs. Rate Escalation – Both can provide real-return durability. Fixed-income vehicles utilize TIPS, CPI swaps, and floating rates. Municipal infrastructure cash flows often include inflation-protective features, such as annual escalators.

Default Dynamics: Corporate Downgrade Risk vs. Essential-Service Stickiness – Essential infrastructure is closer to utility-like cash flow stability, which can behave “bond-like.” Corporate bonds are susceptible to demand loss, competition, and margin compression, whereas essential infrastructure demand is “sticky” because people must consume essential services such as water and electricity.

Price Volatility vs. Fundamental Value Stability – Infrastructure portfolios can exhibit lower mark-to-market volatility. Usage-based cash flows are not subject to market swings or interest rate movements, whereas fixed income vehicles can fluctuate with rates/spreads even if the issuer remains healthy.

Credit Enhancements vs. Structural Protections – Both investment types offer substantive investor protections. Fixed income carries traditional items such as covenants, seniority, reserve accounts and lien/collateral packages. Infrastructure contracts generally include step-in rights, termination payments, and may also include maintenance requirements, enhancing risk protection by ensuring assets remain in a state of good repair, thereby sustaining cash flow generation.

Core Underwriting Discipline

A specific example is modernizing water and wastewater systems through pump station upgrades, treatment plant resiliency, advanced metering infrastructure, and leak detection to address drought, flooding, and aging network risks.

Water and wastewater investments generate predictable, usage-based revenue streams from municipal ratepayers. Unlike many sectors, demand for water is highly inelastic; consumption may fluctuate modestly, but payment priority remains high across economic cycles.

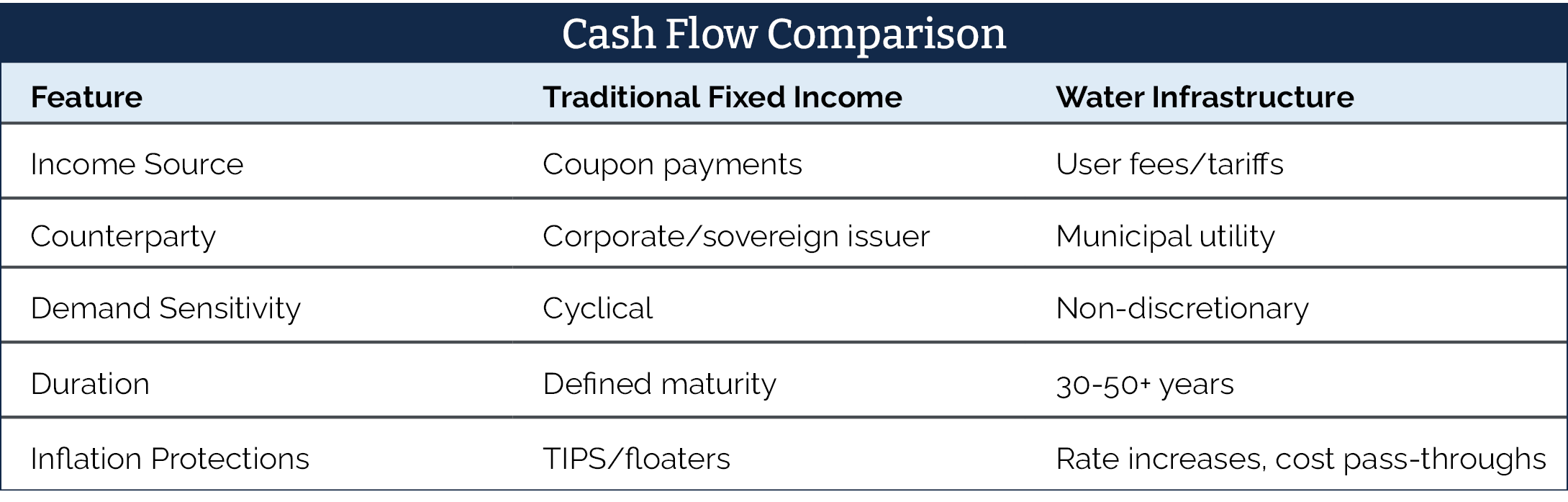

The cash flow comparison to fixed income is instructive:

While simplified, the distinction is important: water assets tend to maintain or increase cash flows as costs rise, whereas nominal bonds can lose real value. These characteristics collectively reduce operational and financial risk — supporting stronger, more stable revenue streams. Additionally, these mechanisms provide a natural hedge against inflation that is often more direct and durable than traditional fixed income instruments. Collectively, these features can provide a level of control and downside protection that exceeds many traditional public bond investments.

Consequently, water infrastructure can serve as a complementary component to fixed income within real asset or inflation-protection allocations, supporting income generation, inflation durability, and long-term risk mitigation for public pension portfolios.

Conclusion

As public pensions continue to evolve their portfolio allocations, usage-based essential infrastructure offers a compelling bridge between fixed income and real assets. Its combination of essential service demand and inflation — linked cash flows makes it uniquely suited to long-term liability matching.

For fiduciaries focused on protecting beneficiaries over decades, that alignment is not just attractive — it is essential.

About the author:

Jason McGaugh serves as Sustainability Partners’ (SP) Chief Capital Officer, responsible for formulating investment processes, project investment theses, transaction structuring, returns analyses, and project risk management for the Company’s $15 billion infrastructure project pipeline.

He leads SP’s utilization underwriting and due diligence activities, including credit risk evaluation and project cash flow analysis.

Prior to joining SP, Jason spent 8 years at the largest renewable energy manufacturing company in the Western hemisphere, responsible for M&A evaluation and strategic financial leadership to multiple business lines.

Prior experience includes 17+ years in investment banking and advisory roles with deal experience exceeding $2 billion of enterprise value across multiple industries, representing domestic and international companies on buy-side, sell -side and capital raise transactions. Mr. McGaugh earned both his Bachelor of Science in Finance and MBA from the W.P. Carey School of Business at Arizona State University and has held numerous Securities licenses throughout his career.